Over the past decade, home insurance costs have risen rapidly in many parts of the United States. This trend has been driven by numerous factors, including an increase in the costs associated with extreme weather events, the COVID-era spike in nationwide housing values, and high inflation rates in 2021 and 2022.

Before 2017, the five-year rolling average cost associated with billion-dollar disaster events was consistently less than $100 billion in the U.S.1 In 2017, three major tropical cyclones (Hurricanes Jose, Irma and Maria), wildfires and several severe storms cost the U.S. more than $390 billion. According to the National Atmospheric and Oceanographic Administration, since 2017, the five-year rolling average cost associated with billion-dollar extreme weather events has exceeded $120 billion.2

This trend of increasing costs due to extreme weather events is likely to continue. Such events are projected to become more frequent and more severe due to climate change,3 creating mounting cost pressures for federal, state, and local governments, as well as insurance companies. Many homeowners, in turn, will experience these cost pressures in the form of increased home insurance premiums.

In some parts of the country, rising insurance costs are already contributing to home affordability challenges. News articles from communities in Florida,4 Iowa5 and Louisiana6 include profiles of homeowners who have been dropped by their insurance carriers and forced to find new policies with premiums that can sometimes be more than twice as expensive as their old coverage. Since 2018, more than 1.9 million insurance contracts have been dropped nationwide, particularly in parts of the country with high wildfire and hurricane risk.7

While those who own their homes outright can forgo insurance entirely (and more and more are),8 for homeowners with mortgages, insurance is an unavoidable cost. Lenders require basic home insurance (also called hazard insurance). Homeowners in areas designated by the Federal Emergency Management Agency as at high flood risk face still higher insurance-related costs, because lenders require them to hold additional flood insurance. Additionally, in some areas, wind and hail damage may not be covered under a homeowner policy and require separate coverage.9

Rising insurance costs — and the associated affordability challenges for homeowners — are likely to have broad effects on the U.S. housing and mortgage market. Home values may fall as fewer prospective homebuyers are able to afford the insurance they need to obtain a mortgage, and home value declines could affect local government revenue streams that depend heavily on property taxes.

Because these impacts are interconnected, insurance cost increases will affect every participant and stakeholder in the U.S. housing and real estate market — from individual homeowners and lenders, to investors, local municipalities and the federal government. In the face of these challenges, it is critical for these stakeholders to understand the trends in insurance costs across the country.

So how are insurance costs changing across the United States?

This is not as simple a question as it may seem. Climate risk is not the only factor that influences home insurance costs. Premiums are also tied to the amount of coverage (often set by the value of the home) and over the past five years, home values, as well as construction and replacement costs, have risen across the country. Between the start of the COVID-19 pandemic in March 2020 and January 2023, single-family home values rose by 36% according to the ICE Home Price Index – a broad measure of housing price change across the country.

As home values increase, the amount of insurance coverage purchased generally also increases — leading to a rise in premiums even if all other factors remain constant. High inflation over the past few years has also contributed to an increase in the dollar amount of insurance premiums paid across the United States.

Below, we examine average insurance cost changes from several different perspectives to tease out the contributions of these different factors. All visualizations and analyses are based on average insurance costs from more than 18 million single-family loans in the ICE McDash data set.10 The ICE McDash data set contains anonymized data on residential loans in the United States going back to 2013, including origination dates, insurance costs, coverage amounts and deductible levels, as well as the zip code of the home. Data on 2025 costs included in this analysis is current through August 2025.

Throughout this analysis, hazard insurance costs refer to the costs for basic home insurance policies (which do not generally include coverage for flood damage), while total insurance costs are calculated as the sum of all annual insurance premiums, including basic hazard insurance, flood insurance, and any additional insurance (earthquake, wind, etc.).

How have insurance costs changed for U.S. homes with continuously existing loans?

Insurance costs associated with continuously existing loans are noteworthy because they reflect costs for the same homes and homeowners through time. In the ICE McDash data set, there are two million loans that existed continuously between December 2014 and August 2025.

In 2014, average total insurance cost for these loans was about $1,230; by 2025, that cost had nearly doubled to $2,440.

Animation 1. Annual average total insurance costs for loans that existed continuously between 2014 and 2025 by county. Source: ICE McDash as of 9/01/2025.

In 2014, average hazard insurance cost per $1,000 of coverage for these loans was about $5.50; by 2025, this cost had increased to about $6.70 per $1,000 of coverage.

Animation 2. Average costs by county to purchase $1,000 of hazard insurance for loans that existed continuously between 2014 and 2025. Source: ICE McDash as of 9/01/2025.

Figure 1. Average costs for continuously existing loans over time. Source: ICE McDash as of 9/01/2025.

Recent patterns of rising insurance costs — impacted by a confluence of factors that include extreme weather event losses, housing value changes and inflation — are especially clear when mapped by state between 2019 and 2025. Over this time period, Florida and Louisiana had the largest average absolute change in the cost per $1,000 of coverage for continuously existing loans in the ICE McDash data set.

Figure 2. Changes in average insurance costs per $1,000 of coverage for continuously existing loans by state between 2019 and 2025. Source: ICE McDash as of 9/01/2025.

How have insurance costs changed for U.S. homes with loans originated in 2014 and 2024?

The value of looking at insurance costs for originated loans each year is that these costs reflect the insurance market as of that year. Changes in insurance costs for newly originated loans each year may reflect increases due to recently assessed housing value and the implementation of the National Flood Insurance Risk Rating 2.0 Program starting in 2021, an effort to bring flood insurance premiums more in line with risk.

In the ICE McDash data set, there are 950,000 loans originated in 2014, peaking at 3.6 million loans originated in 2021, before declining to about one million loans originated in 2024. (As of August 2025, only about 714,000 loans in the ICE McDash data set had been originated year to date, so though we show changes through August 2025 in the figures below, we focus on costs for newly originated loans through only 2024 in the text.) In 2014, average total insurance cost for these loans was about $1,150; by 2024, it was $1,950.

Animation 3. Annual average total insurance costs for loans originated in each year between 2014 and 2025 by county. Source: ICE McDash as of 9/01/2025.

In 2014, average hazard insurance cost per $1,000 of coverage for these loans was about $4.70; by 2024, it was about $5.40. Importantly, these costs per $1,000 of coverage are significantly lower than costs for continuously existing loans — please see the section “To what extent could shopping around for insurance policies reduce costs?” below for an in-depth analysis of these differences.

Animation 4. Average costs by county to purchase $1,000 of hazard insurance for loans originated in each year between 2014 and 2025. Source: ICE McDash as of 9/01/2025.

Figure 3. National average costs for originated loans in ICE McDash each year from 2014 to 2025. Source: ICE McDash as of 9/01/2025.

How have insurance costs changed for all U.S. homes with active loans?

This cross-section of loans represents the broadest view of insurance cost increases. In the ICE McDash data set, there are about 12 million single-family loans that were active in 2014 and about 18 million active single-family loans in 2025.

In 2014, average total insurance cost for these loans was about $1,270; by 2025, it was $2,405.

Animation 5. Annual average total insurance costs for all active loans each year between 2014 and 2025 by county. Source: ICE McDash as of 9/01/2025.

In 2014, average hazard insurance cost per $1,000 of coverage for these loans was about $5.40; by 2025, it was about $6.10. Total insurance costs per $1,000 of coverage was about $0.20 higher than hazard insurance alone.

Animation 6. Average costs by county to purchase $1,000 of hazard insurance for all active loans in each year between 2014 and 2025. Source: ICE McDash as of 9/01/2025.

Figure 4. Average insurance costs for all active single-family loans in the ICE McDash data set over time. Source: ICE McDash as of 9/01/2025.

Have insurance costs increased if we account for inflation?

The U.S. dollar’s buying power in 2025 is weaker than it was in 2019. To understand the impact of inflation on insurance costs, we can compare the difference in total insurance costs between 2019 and 2025 using both nominal dollar amounts in each year and inflation-adjusted dollars (adjusted to USD in 2025). The year 2019 was chosen to represent costs pre-pandemic.

Miami-Dade County, Florida, provides a particularly striking example. The average total insurance cost increase between 2019 and 2025 in Miami-Dade is more than $900 lower in inflation-adjusted dollars than it is in nominal dollars (accounting for inflation makes a progressively larger difference farther back in time). In percentage terms, the annual increase in total insurance costs in nominal dollars exceeded 13% in 2022, but when inflation adjusted, the increase was only about 5.5% (Figure 5).

Figure 5. Total insurance costs in Miami-Dade County in nominal and inflation-adjusted dollars for all active loans (left). Percent annual change in costs in nominal and inflation-adjusted dollars for all active loans (right). ICE McDash as of 9/01/2025.

Nationwide, the pattern is similar. Inflation has been a major contributing factor to increasing insurance costs between 2019 and 2025. In quantitative terms, inflationary pressure accounts for about 33% ($335) of the nominal dollar insurance cost change over this period ($1,000; Figure 6).

Figure 6. Average change in total insurance cost from 2019 to 2025 for all active loans across the country in nominal dollars (left). Average change in total insurance cost from 2019 to 2025 for all active loans across the country in inflation-adjusted 2025 dollars (right). Source: ICE McDash as of 9/01/2025.

After accounting for inflation, insurance costs increased in every county in the country, except for 12 counties. Some of the regions with the largest insurance increases in inflation-adjusted dollars are Florida, the greater New Orleans region of Louisiana, northern Texas and northern Colorado.

Have U.S. home insurance costs increased after accounting for both coverage amount changes and inflation?

Both inflation and the amount of coverage purchased by homeowners have had a significant impact on insurance costs, but the cost to purchase $1,000 of insurance is not dependent on inflation. In this analysis, we estimate what insurance costs would be in 2025 if the 2019 cost per $1,000 of coverage were applied to 2025 hazard coverage amounts.

For example, in Miami-Dade County, Florida, the average cost to purchase $1,000 of hazard insurance was about $16.20 in 2019 and $17.30 in 2025 across active single-family loans in the ICE McDash data set. To put this in perspective, if the cost per $1,000 of coverage had remained fixed at 2019 levels in Miami-Dade County, the anticipated average hazard insurance cost in the county would be about $385 lower than it actually is in 2025 (based on the $344,530 average coverage amount in the county in 2025). This additional $385 represents the increase in insurance costs in Miami-Dade County after accounting for both inflation and increased coverage amounts.

Nationwide, a similar trend holds true: if the cost per $1,000 of hazard insurance coverage remained constant from 2019 to 2025, the anticipated average hazard premium in 2025 would be about $355 cheaper (or about 0.80 cents cheaper per $1,000 of coverage) than it actually is.

Figure 7. Differences between actual hazard premiums in 2025 and anticipated premiums in 2025 for all active loans based on the cost to purchase $1,000 of insurance coverage in 2019 (county averages). Anticipated premiums apply the 2019 cost per $1,000 of insurance coverage to 2025 coverage amounts. Source: ICE McDash as of 9/01/2025.

Figure 8. Differences between cost per $1,000 of coverage in 2025 and cost per $1,000 of coverage in 2019 for all active loans (county averages). Source: ICE McDash as of 9/01/2025.

There is significant geographic variation in the difference between anticipated premiums in 2025 based on 2019 costs and actual costs across the country. For many homeowners, however, it is the nominal dollar increases in insurance costs that matter most in terms of affordability. The analyses and visualizations above provide a more nuanced view of these trends, illuminating shifts that may be at least partially attributable to increasing climate-related insurance losses.

To what extent could shopping around for insurance policies reduce costs?

ICE explored changes in average insurance costs in the United States through time for three groups of loans within the ICE McDash data set.11 The differences in cost trends between these three cross-sections of loans suggest that homeowners could save hundreds of dollars every year by shopping around and getting multiple home insurance quotes. To understand this, it is helpful to think about the homeowners represented in these three loan cross-sections:

- The roughly two million loans that existed continuously between December 2014 and June 2025. These loans are associated with established homeowners. Unless dropped by an insurance carrier, these households are not likely to shop around or negotiate for cheaper or better policies each year. Nor are they likely to increase their deductibles to match increases in coverage as their house gains value.

- Loans that were originated in each year from 2014 to 2025.12 The number of mortgages in this sample ranges from 950,000 loans originated in 2014 to 3.6 million loans originated in 2021. Homebuyers associated with these newly originated loans are likely to have been actively engaged in insurance policy selection in that year, making decisions around deductible amounts and perhaps receiving multiple quotes.

- All active loans each year from 2014 to 2025.13 The number of active single-family loans in the ICE McDash data set has increased over time, from about 12 million in 2014 to 18 million in 2025. This cross-section of loans represents the most holistic view of insurance costs that we have for homeowners across the country.

The figure below shows the average cost to purchase $1,000 of coverage for each of the three loan cross-sections from 2014 to 2025. Though data for 2025 is shown below, we focus on the period between 2014 to 2024 because we only have a partial picture of 2025. As of August 2025, there are only about 700,000 originated loans in 2025 in the ICE McDash data set.

Loans that were continuously in existence from 2014 to 2024 have higher average costs than newly originated loans every year. Indeed, in any given year, homeowners with loans that were continuously in existence often spent in excess of a dollar more per $1,000 of insurance coverage than homeowners with newly originated loans. This adds up quickly: for $400,000 in insurance coverage, it equates to an additional $400 annually in insurance costs.

Figure 9. Average hazard insurance costs per $1,000 of coverage over time for three loan cross-sections. Source: ICE McDash as of 9/01/2025.

In 2024, insurance costs for continuously existing loans were about $1.20 more per $1,000 of coverage than newly originated loans. The average cost per $1,000 of coverage of originated loans in 2025 ($5.40) is only about 10 cents less per $1,000 of coverage than continuously existing loans in 2014 ($5.50). In other words, by actively engaging in insurance policy selection every year — as new homebuyers and loan applicants tend to do — homeowners with longstanding loans could potentially rewind their average insurance costs per $1,000 of coverage by nearly a decade.

How have hazard deductibles changed over time for U.S. homeowners?

Hazard deductibles have steadily increased over time. For active single-family loans in the ICE McDash data set, the average hazard deductible was about $1,450 in 2019; by 2025, it is about $2,000.

Figure 10. Hazard deductible selected for all active loans in 2019 and 2025. Source: ICE McDash as of 9/01/2025.

Continuously existing loans tend to have lower deductibles, most likely because homeowners do not always increase their deductible amount to match home appreciation values (Figure 11). Historically, common deductibles are either set as fixed amounts (e.g., $500 or $1,000) or as a percentage of coverage amount (typically 0.5% to 1.5%).

Figure 11. Average hazard deductibles through time for three types of loan cross-sections. Source: ICE McDash as of 9/01/2025.

Looking at hazard deductibles as a percentage of hazard insurance coverage amount, the story is more complicated. Starting in 2021, there seems to be a distinct difference in behavior (in terms of deductible selection) between new policyholders and existing homeowners. New homebuyers seem to be systematically adjusting their deductibles upward to reduce insurance premium costs, while existing homeowners are not proactively making this shift, even as coverage amounts increased during the pandemic’s housing boom (Figure 12). In 2024 and 2025, it appears that some existing homeowners may have begun proactively increasing their deductible amounts to offset rising costs.

Figure 12. Hazard deductible as a percentage of coverage amount over time for loans originated in each year, loans that existed continuously between 2014 and 2025, and all active loans in each year. Source: ICE McDash as of 9/01/2025.

What do these changes look like on a state-by-state basis?

In 2025, Louisiana, Oklahoma, and Florida had the highest average statewide insurance costs in the country, with the average cost across all active loans at $11.75 in Louisiana and over $10 in Oklahoma, Florida and Nebraska. Nationwide, the average cost per $1,000 of hazard coverage was $6.10 in 2025 for all active loans — nearly half the average costs in Louisiana. Homeowners in Louisiana, Nebraska and Florida have also seen some of the largest increases in hazard insurance costs (per $1,000 of coverage) for active single-family loans since 2019.

Figure 13. Cost to purchase $1,000 of insurance in Florida statewide and in Miami-Dade County from 2014 to 2025 for different cross-sections of loans. Source: ICE McDash as of 9/01/2025.

Costs start to increase in Florida more rapidly after Hurricane Irma and Hurricane Michael hit the state in 2017 and 2018, respectively. In Louisiana, costs seem to increase more rapidly starting in 2021 after Hurricane Ida.

Figure 14. Cost to purchase $1,000 of insurance in Louisiana and New Orleans Parish from 2014 to 2025 for different cross-sections of loans. Source: ICE McDash as of 9/01/2025.

California homeowners, by contrast, have some of the least expensive insurance rates in the nation over the past 10 years (Figure 15). California’s rate regulation process is complex — for example, insurers need the approval of the state insurance regulator to set rates and consumers can challenge annual rate increases higher than 7%.14

Until 2023, the state did not allow forward-looking models to be used in setting rates, only historical data, and also did not allow insurers to incorporate their reinsurance costs into insurance rates. The state announced efforts to loosen these regulations in late 2023 after State Farm and Allstate stopped issuing policies in the state following several years of significant wildfire losses, including the Camp Fire that destroyed Paradise, California, in 2018.15

Figure 15. Cost to purchase $1,000 of insurance in California from 2014 to 2025 for different cross-sections of loans. Note that the y-axis is different from above. Source: ICE McDash as of 9/01/2025.

Do state regulations lead to systematic differences in insurance costs?

As mentioned above, the U.S. insurance industry is regulated on a state-by-state basis. When an insurance company wants to change its rates, it must submit a rate proposal to state regulators for review and approval. In some states, this can be a slow process, with months between the initial submission and its implementation; in others, regulators usually grant approval to the proposed increases, and the new rates are applied to any new policies issued or renewal of an existing policy. Since homeowners insurance is required to obtain a mortgage, there is often political pressure on state governments to make sure rates are affordable and available to residents.

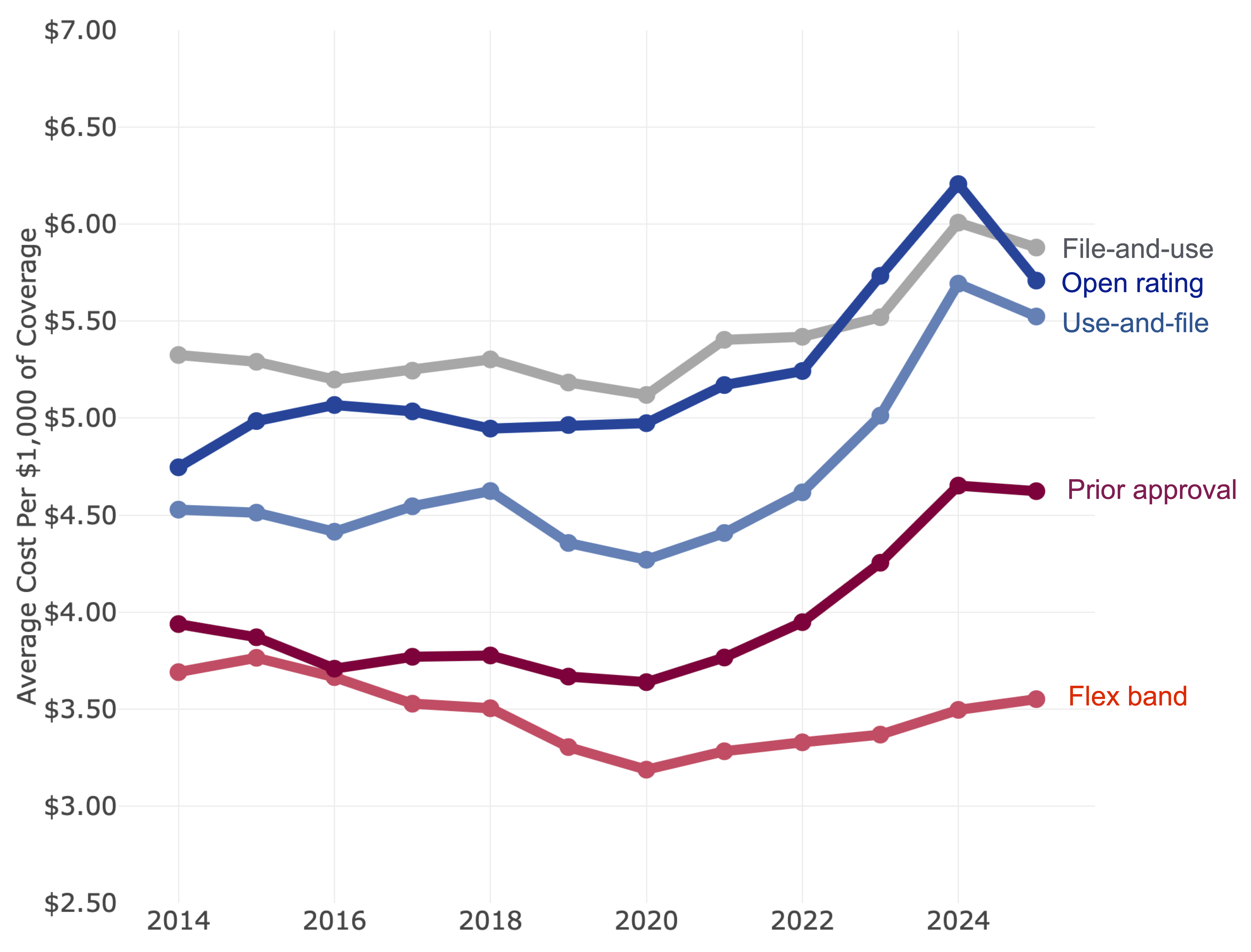

The U.S. Treasury Department identifies five main types of state rate regulation (Figure 16):16

- Open rating: insurers set rates and state regulator intervention is limited

- Use-and-file: insurers set rates for their products but must file with state regulators, who review and may intervene within a given period

- File-and-use: insurers must file a rate request with a state regulator and the regulator has a certain amount of time to approve or deny it; if the regulator takes no action during the period, the insurer can make the rate change

- Flex band: insurers may use-and-file for rate increases that are less than a certain amount, but must obtain prior approval for larger rate increases

- Prior approval: insurers must file rate requests with state regulators and obtain prior approval to change rates

Figure 16. State insurance rate regulatory regimes. Source: Federal Insurance Office Report, U.S. Department of the Treasury.17

By looking at the average insurance cost per $1,000 of coverage across active loans in the states in each regulatory regime through time, it is clear that regulations do play a significant role in insurance costs. States with “looser” regulations (open ratings and file-and-use) tend to have systematically higher insurance costs than states with prior approval and flex band systems.

Insurance costs by state regulatory regime

Figure 17. Average insurance costs for all active single-family loans through time in the ICE McDash data set by state insurance rate regulatory regime. Source: ICE McDash as of 9/01/2025.

Conclusion

Patterns of home insurance costs and cost changes across the United States since 2014 illuminate the complexity of the insurance-related challenges facing the U.S. housing and mortgage markets. One of ICE’s central goals is to help increase transparency in global financial markets, connecting investors and financial market participants with the data they need to assess risks and make informed decisions. By teasing apart the impact of hazard deductibles, inflation, coverage amounts, state regulation and loan types, mortgage market participants can gain a more holistic and nuanced view of insurance cost changes taking place across the country.

1 These totals are Consumer Price Index-adjusted.

2 Billion-dollar Weather and Climate Disasters. National Centers for Environmental Information. National Oceanographic and Atmospheric Administration. Available at: https://www.ncei.noaa.gov/access/billions/state-summary/US

3 S, S.I et al (2021)/ Weather and Climate Extreme Events in a Changing Climate. In Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [Masson-Delmotte, V., et al. (eds.)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA, pp. 1513–1766, doi: 10.1017/9781009157896.013. Available at: https://www.ipcc.ch/report/ar6/wg1/chapter/chapter-11

4 Colin, M & Tracy M (17 Oct 2024). Florida homeowners fear soaring insurance cost after hurricanes. Reuters. Available at: https://www.reuters.com/world/us/florida-homeowners-fear-soaring-insurance-cost-after-hurricanes-2024-10-17

5 Bolton, S (24 Oct 2024). Iowa homeowners reel from doubling insurance rates amid inflation, storms. KTVO.com. Available at: https://ktvo.com/news/local/iowa-homeowners-face-shocking-insurance-rate-hikes-amid-economic-challenges

6 Meyersohn, N & A Bahney (26 Apr 2024). The home insurance market is crumbling. These owners are paying the price. CNN. Available at: https://www.cnn.com/2024/03/29/economy/home-insurance-prices-climate-change/index.html

7 Flavell, C & Rojanasakul M (2024). Insurers Are Deserting Homeowners as Climate Shocks Worsen. The New York Times. Available at: https://www.nytimes.com/interactive/2024/12/18/climate/insurance-non-renewal-climate-crisis.html

8 Cooley, P. (27 May 2024). Home insurance was once a ‘must.’ Now more and more homeowners are going without. The Washington Post. Available at: https://www.washingtonpost.com/business/2024/05/27/home-insurance-dropped-coverage

9 Texas Department of Insurance. Home Insurance: What structures are covered? Available at: https://www.tdi.texas.gov/tips/home-insurance-structures-covered.html

10 Loans that cannot be matched to a zip code-level location are excluded from this analysis. Data from counties that contain five loans or less is also excluded. ICE McDash data consists of loan level insurance costs in December of every year from 2013 to 2022, as well as monthly data from 2023 onward.

11 Loans that cannot be matched to a zip code-level location are excluded from this analysis.

12 Through November 30, 2024.

13 Through November 30, 2024.

14 Frank, T (E&E News from Politico https://www.eenews.net/articles/calif-scared-off-its-biggest-insurer-more-could-follow

15 Webel, B. (2 Nov 2023). The Factors Influencing the High Cost of Insurance for Consumers. Statement before the Committee on Financial Services Subcommittee on Housing and Insurance U.S. House of Representatives. Available at: https://crsreports.congress.gov/product/pdf/TE/TE10087

16 Federal Insurance Office, U.S. Department of the Treasury. Analyses of U.S. Homeowners Insurance Markets, 2018-2022: Climate-related risks and other factors. Appendix A, Table 3 (“State Insurance Rate Regulatory Regimes by Region”) p 48. Available at: Analyses of U.S. Homeowners Insurance Markets, 2018-2022: Climate-Related Risks and Other Factors (January 2025)

17 Federal Insurance Office, U.S. Department of the Treasury. Analyses of U.S. Homeowners Insurance Markets, 2018-2022: Climate-related risks and other factors. Appendix A, Table 3 (“State Insurance Rate Regulatory Regimes by Region”) p 48. Available at: Analyses of U.S. Homeowners Insurance Markets, 2018-2022: Climate-Related Risks and Other Factors (January 2025)

More about the data

These visualizations and analyses are based on data from ICE McDash, including origination dates, insurance costs, coverage amounts and deductible levels for millions of active loans in the United States. This data goes back to 2013 and covers costs for standard hazard insurance policies, flood insurance, earthquake insurance, and any additional insurance purchased for the home such as wind, hail, and wildfire coverage. Somewhat confusingly, the phrase “hazard insurance” often refers to standard homeowner insurance policies, while earthquake, flood, and other kinds of policies are referred to as “additional coverage.” We follow this terminology throughout these analyses.

ICE McDash data consists of loan level insurance costs in December of every year from 2013 to 2022, as well as monthly data from 2023 onward (through August 2025). Unless otherwise noted, costs are calculated at the loan level (such as the cost to purchase $1,000 worth of coverage and the total insurance costs) before being aggregated to zip codes. The average insurance costs of all loans within a zip code are aggregated up to county averages. County estimates are based on average costs, weighted by the number of loans in each zip code.

Limitations

This document contains information that is proprietary property of Intercontinental Exchange, Inc. and/or its affiliates (“ICE Group”), is not to be published, reproduced, copied, modified, disclosed or used without the express written consent of ICE Group.

This material is provided for informational purposes only. The information contained herein is subject to change without notice. Nothing herein should in any way be deemed to alter the legal rights and obligations contained in agreements between ICE Group and its clients relating to any of the products or services described herein. Some of the information described herein is still in development and as such, pursuant to ICE Group’s sole discretion, the services and/or methodologies that may ultimately be developed may deviate from the description included herein or may not be developed at all. Nothing herein is intended to constitute legal, tax, accounting, investment or other professional advice.

ICE Group makes no warranties whatsoever, either express or implied, as to merchantability, fitness for a particular purpose, or any other matter. Without limiting the foregoing, ICE Group makes no representation or warranty that any data or information (including but not limited to evaluations) supplied to or by it are complete or free from errors, omissions, or defects and nothing contained herein should constitute any form of warranty, representation, or undertaking.

All feature values included in the products and services described herein are estimates, including those values that are derived using data provided by other data providers as well as forecasts of expectations of change. Such estimates are based upon information available to ICE Group at the time of calculation, are provided as is, and should be treated as estimates and forecasts with potentially substantial deviations from actual outcomes, regardless of whether such features are explicitly described in any data dictionary, methodology, or definition as estimates or forecasts.

Where required, the features are developed using a set of methodologies designed to prevent any form of reverse engineering or geographic identification from the features in isolation or in combination but still provide potentially meaningful insights regarding the underlying securities.

ICE Group is not registered as a nationally registered statistical rating organization, nor should this document be construed to constitute an assessment of the creditworthiness of any company or financial instrument. Analytics available through the service are meant to be generally indicative of overall feature sets and should not be considered an analyst’s opinion of the underlying investability of a particular location or security. These analytics are designed to help summarize and aggregate large amounts of information, but will therefore not capture the nuances, or the “full picture” of any entity’s features. No part of this service should be construed as providing investment advice. Listing or linking to sources in attribution does not indicate endorsement by ICE Group of the data source, nor does it reflect an endorsement by the data provider of the products or services described herein.

GHG emissions information available is either compiled from publicly reported information or estimated, as indicated in the applicable product and services.

ICE Data Services refers to a group of products and services offered by certain Intercontinental Exchange, Inc. (NYSE:ICE) companies and is the marketing name used for ICE Data Services, Inc. and its subsidiaries globally, including ICE Data Indices, LLC, ICE Data Pricing & Reference Data, LLC, ICE Data Services Europe Limited and ICE Data Services Australia Pty Ltd. ICE Data Services is also the marketing name used for ICE Data Derivatives, Inc., ICE Data Analytics, LLC certain other data products and services offered by other affiliates of Intercontinental Exchange, Inc. (NYSE:ICE).

Trademarks of Intercontinental Exchange, Inc. and/or its affiliates include: Intercontinental Exchange, ICE, ICE block design, NYSE, ICE Data Services, ICE Data and New York Stock Exchange. Information regarding additional trademarks and intellectual property rights of Intercontinental Exchange, Inc. and/or its affiliates is located at www.intercontinentalexchange.com/terms-of-use. Other products, services, or company names mentioned herein are the property of, and may be the service mark or trademark of, their respective owners.

© 2025 Intercontinental Exchange, Inc.