Welcome to ICE Data Services’ new “Data Driven Risk Management” series. We’ll be sharing insights into how technology and data are driving new techniques for risk management and bringing modernization to the financial industry. Our focus will be various areas of risk management (e.g. market risk, credit risk, etc.) imparting our experience with the role of data, what we’re hearing across our client base, and data in relation to regulatory requirements and their nuances.

For this post, let’s look at data-driven liquidity risk management programs. Firstly, a financial instrument’s liquidity can be assessed on three key factors - volume, time and price.

How much am I looking to transact?

How long do I have to transact?

What price haircut am I willing to take for immediacy?

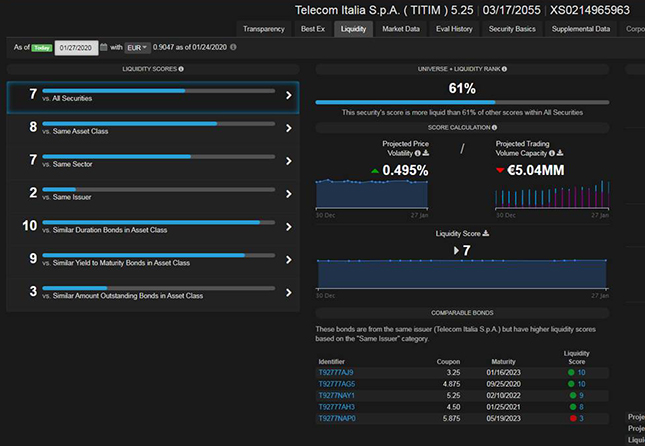

In theory, an appropriate measurement of liquidity would be to consider two of these factors as inputs and quantitatively solve for the third. For example, given a specific volume I own and a price impact that I’m willing to assume, how long would it take to liquidate the holding? Alternatively, if I have a specified time horizon to liquidate the holding with a given price impact, what is the maximum volume I can transact given these parameters? The table below shows how this could work in practical application for a Telecom Italia bond - using data and analytics to understand the liquidity of this fixed income instrument.

Now, let’s take a look at substantial differences in one’s ability to perform these calculations for an exchange-traded equity versus an over-the-counter fixed income bond.

The equity markets have a longer history with data-driven liquidity risk management techniques. When a central limited order book (“CLOB”) market structure and depth of order details are available, it is generally more straightforward and industry-accepted to use data for liquidity analysis. For example, with standards such as VWAP (volume-weighted average price) and ADV (average daily volume), investors can determine a price impact for executing a concentrated volume of a particular stock.

Don’t get me wrong - there are still thinly traded common stocks, OTC equities or pre-IPO scenarios where assessing liquidity may need to be more model-based and where it’s definitely harder to quantify liquidity. Virtually the entire fixed income markets would fall into this category.

Individual companies with tradeable equity are counted in the thousands - the number of fixed income instruments measures in the millions. Less than 2% of outstanding US dollar debt changes hands on any given day, and various characteristics need to be considered to properly assess liquidity (e.g. duration, remaining term to maturity, issuer, etc.). Within many fixed income markets, there is also a ‘fungibility’ - in other words, one doesn’t need to see a particular bond trade to know that it has the potential to trade given observability in certain comparable bonds with similar characteristics.

This concept is paramount to ICE Data Services’ approach to quantitatively measuring liquidity - that every financial instrument has a future trade volume capacity - whether based on recent, observable trading history or whether modelled based on regressions that measure how much of that instrument the market can absorb without significantly affecting the price. These new technologies and improved organization of market data can help the industry by bringing data-driven liquidity risk management to asset classes and market structures that historically were only available in equity markets.