Data in Action

Liquidity and swing pricing during volatile markets

March 16, 2022

David Varano

ICE Data Services Director, Business Development

Pedro Geri

ICE Data Services Director, Business Development

Paul Graham

Director, Fixed Income Sales Specialists, EMEA

We are only three months in, and 2022 is proving to be an eventful year. From Russia’s invasion into Ukraine, to the volatility associated with the onset of another monetary tightening policy, to the inflationary pressures building up across economies around the world, investors and market participants have been reacting strongly to these developments. In bond markets alone, we have seen the ICE BofA MOVE Index, which measures bond volatility, hit its second highest level in 10 years — only the COVID-19 market disruption of March 2020 surpassed it.

During this period of increased volatility, market participants understandably are looking for additional ways to monitor and manage risk. Fund managers experiencing large net outflows may choose to implement swing pricing to help protect existing investors from potential dilution that can be a byproduct of increased fund redemptions that occur during periods of market stress. The process works by adjusting a fund’s net asset value (NAV) per share to pass on the purchasing or redeeming costs associated with those activities. For example, large redemptions in a fund, especially one holding less liquid securities, could force a manager to sell certain less liquid securities at a concession to attract buyers. Swing pricing seeks to minimize the negative economic impact for shareholders who stay invested, and reduce arbitrage opportunities for those who exit, especially during more volatile periods.

In our example below, we take a look at how a fixed income fund might take swing pricing into account and what it might look like in practice for a fund that was invested in emerging markets, including Eastern European countries, like Poland, Czech Republic and Hungary. In our example, we used the ICE BofA Euro Emerging Markets Corporate Plus Index as a benchmark and proxy for the portfolio. The index, which is a subset of the ICE BofA Emerging Markets Corporate Plus Index, including all securities denominated in euro, has experienced a significant uptick in volatility, which has manifested itself in 1-day price returns for the entire fund of -1% to -2% for several trading sessions in early/mid-March. The 1-day price return for the benchmark for the past year can be seen below.

ICE BofA Euro Emerging Markets Corporate Plus Index

Price Return % 1-day-LOC

Source: ICE Data Services, March 3, 2022

In addition to increased asset price volatility, our hypothetical fund manager is likely also dealing with increased investor redemptions, creating a need to raise cash. However, changing market conditions may lead to higher than anticipated costs associated with fulfilling those redemptions.

Typically, a fund manager may elect to apply a swing pricing adjustment factor to the NAV or the settlement price for investors leaving the fund when a fund’s net outflows breach a pre-determined threshold set forth in a fund’s swing pricing policy. Many funds will generally set their threshold in a range somewhere between 2% and 5% of assets under management (AUM) but will regularly review and manage that number. Managers consider many factors when trying to determine an appropriate NAV adjustment factor, including, high-quality, real-time price information which helps gauge the current market’s bid side as a starting point. Also, having dynamic bid/ask spread data that is updated in real-time, and at the security level, serves as a measure of transaction costs. Fund managers can use ICE’s Continuous Evaluated Pricing (CEPTM) to obtain these useful metrics to help establish their swing pricing threshold. Additionally, a liquidity risk model, such as ICE’s Liquidity IndicatorsTM service, that captures the non-linear nature of trading can assist fund managers in determining an appropriate swing price adjustment factor. In other words, capturing that most markets experience a decreasing rate of transaction volume that can be achieved at a given market price.

If our hypothetical fund manager above has AUM of €1.0 billion and would like to apply swing pricing on days when net outflows range from 2% to 5%, using ICE Liquidity Indicators, we can estimate the cost of raising between €20 million and €50 million to fulfill those redemptions. From that we can calculate the appropriate swing price adjustment factor needed to protect remaining investors from dilution. After uploading the fund’s holdings, position sizes, and liquidation volumes, we can generate output at the fund (i.e., the portfolio) level. In this hypothetical example we used a pro-rata strip of the entire index, indicating a total cost to liquidate stood between €81,286 to €179,669. ICE Liquidity Indicators enables users to break down the total cost into two components: the transaction cost, which is calculated from bid/ask spreads, and the market price impact, which is calculated from our Liquidity Indicators service, factoring in the non-linear aspect of the market described above.

The market price impact model may incorporate any of the following variables depending on asset class: The Bid-Ask spread of the bond; the projected price volatility of the bond; an inflation variable, comparing volume required to perform a trade in a given time constraint relative to the "normal" daily trade volume capacity; an ICE evaluated bid price of the bond; or an asset class specific constant (intercept in the regression model). These variables get updated daily based on market conditions, using a regression model built by comparing day-over-day volume weighted trade price changes to the variables listed above.

Liquidation Cost Analysis

Source: ICE Data Services, March 10, 2022

Since financial market conditions can deteriorate quickly during times of stress, it is helpful for fund managers to have the ability to consider a range of appropriate swing price thresholds and a clearer picture of what the general appetite for risk might look like if and when large scale liquidations may be required. ICE Liquidity Indicators offers customers the ability to conduct scenario analysis, using pre-defined stress simulations (e.g., the 2008 Financial Crisis, the COVID-19 crisis, etc.) or customized settings for hypothetical simulations. As part of this functionality, users can adjust the base case variables — such as implied price volatility, bid/ask spreads, trade volume capacity (i.e., a proxy for market accessibility) — to create more conservative or more aggressive environments. For our hypothetical portfolio, the “Moderate” stress and “Adverse” stress scenario, shows that at a 3% swing price threshold, the cost to liquidate rises from €106,875 in the base case to €196,580 and €230,857 for moderate and adverse scenarios, respectively.

Source: ICE Data Services, March 10, 2022

While swing pricing adjustments are implemented at the fund level, it is beneficial for fund managers to understand what is going on “under the hood” to understand what is driving the fund level outputs. Through the ICE VantageTM user interface, ICE Liquidity Indicators displays important metrics (both current and historical) of an individual security’s liquidity profile, which allows for a bond-by-bond comparison. These metrics can assist fund managers in their calculation and management of the NAV factor and also to understand the differences and anomalies that may justify further examination.

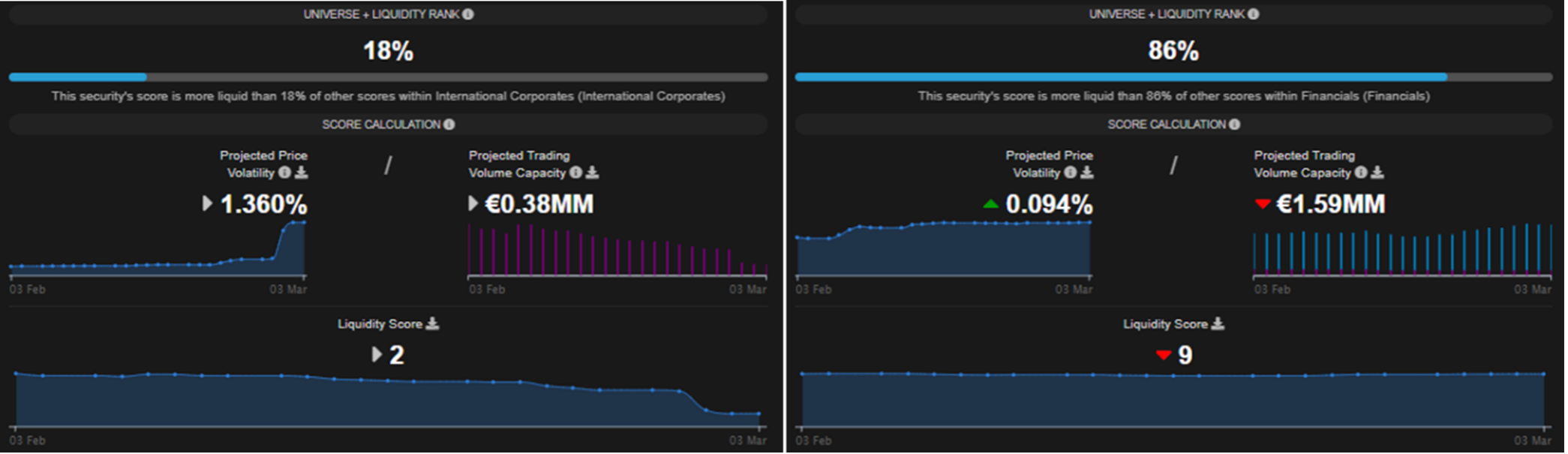

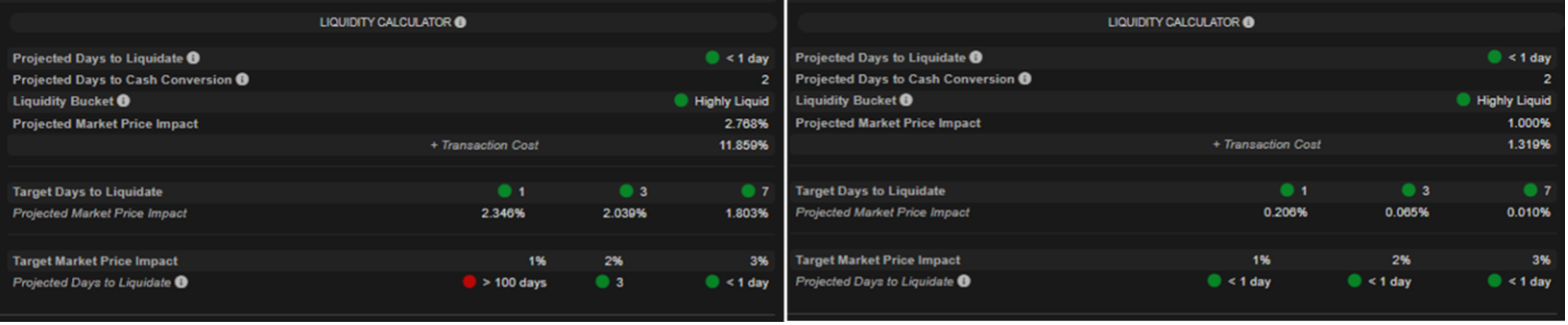

From the more than 200 constituents of the ICE BofA Euro Emerging Markets Corporate Plus Index, using ICE Liquidity Indicators, we examined two bonds with very different profiles to highlight how a fund manager could use these analytics to dive deeper into security-specific details. In this example, Bond A exhibits a less liquid disposition than Bond B, as evidenced by the much lower liquidity score (2 versus 9), higher projected price volatility (1.36% versus 0.09%), and lower projected trading volume capacity (€380,000 versus €1,590,000). Additionally, the ICE Liquidity Indicators service offers clients the flexibility to use their own assumptions to drive output via the liquidity calculator. In our example, Bond A has a base case projected market price impact of 2.77% and a transaction cost of 11.85%, while Bond B has 1.00% and 1.14%, respectively. Armed with these additional, security-specific liquidity analytics, a fund manager could elect to adjust a liquidation program beyond what a pro rata calculation would suggest, in order to attempt to limit transactional costs for the entire fund.

Source: ICE Data Services, March 10, 2022

Market conditions can be a moving target, calm and steady for weeks or months on end, but then suddenly distressed. When considering how to construct the proper policy for applying swing pricing, fund managers can benefit from high quality inputs and robust procedures. ICE’s Continuous Evaluated Pricing offers real-time bond price data including dynamic bid/ask spread information, driven by an approach that combines both systematic and human analysis. ICE’s Liquidity Indicators provides an independent assessment of liquidity risk for approximately 4.6 million investment instruments across a wide range of asset classes. Among other things, it assigns a liquidity score to individual securities and provides estimates of trade volume capacity, future price volatility, days to liquidate, market price impact liquidation costs and more.