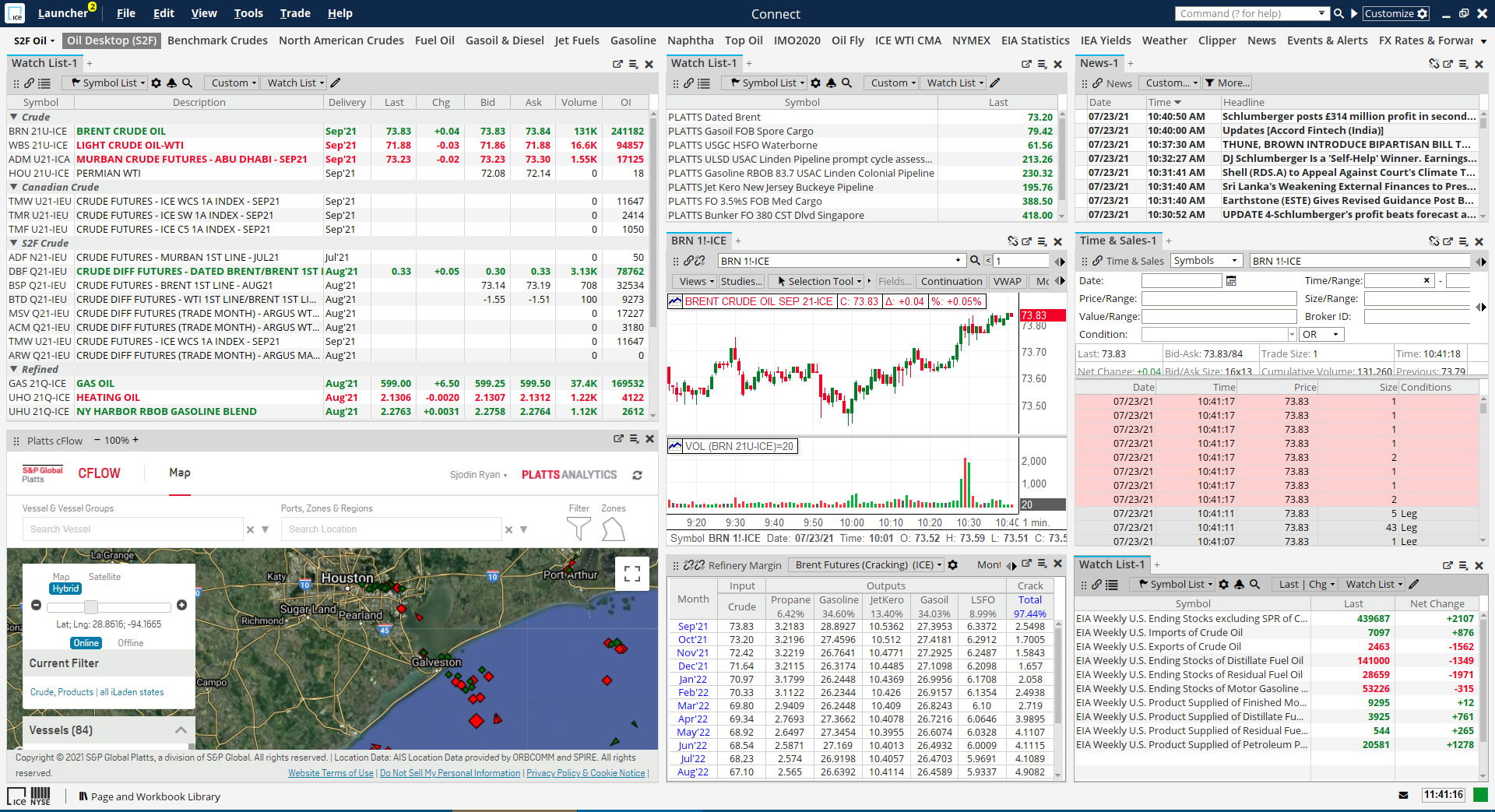

The power of S&P Global Energy cargo tracking and trade flows, refining, storage data, price assessments, forward curves and commodity market insights enhances the ICE Connect messaging, data, and execution platform capabilities. Traders, analysts, and risk managers can effectively manage their workflows from a single platform to get a fresh perspective on the oil markets to quickly make informed decisions. This collaboration between ICE and S&P Global Energy is positioned to support analyses of the global energy and commodities markets, giving fresh perspectives, and facilitating new opportunities to explore.

S&P Global Energy

Our expanded offering provides a full view of the energy markets, from energy transition to supply chain data, as well as our core pricing and news platform

Powered by S&P Global Energy

Click image to enlarge

S&P Global Energy

Cargo tracking and trade flows

Upgrade your vessel tracking service with the addition of S&P Global Energy (Shipping Service) to access essential cargo information on oil tankers as they leave a port including terminal of origin and destination, ETAs, quantity, grade, and charter party information to identify opportunities and trading decision and support commodity flows. Monitor volumetric crude oil exports and imports as it happens and discover shifting market trends before anyone else.

World refinery database

Access the Platts World Refinery Database for in-depth views of the global refining industry, including capacity data by unit and configuration, ownership status and history, and refinery-by-refinery crude slate, yields and outages data.

Oil inventory

Monitor and analyze this comprehensive global inventory database, covering detailed crude and refined petroleum inventories data - recent and historical. A combination of proprietary Analytics and third-party data, curated by S&P Global Energy, provides access to highly sought-after fundamentals.

Cargo tracking and trade flows

Upgrade your vessel tracking service with the addition of S&P Global Energy (Shipping Service) to access essential cargo information on oil tankers as they leave a port including terminal of origin and destination, ETAs, quantity, grade, and charter party information to identify opportunities and trading decision and support commodity flows. Monitor volumetric crude oil exports and imports as it happens and discover shifting market trends before anyone else.

World refinery database

Access the Platts World Refinery Database for in-depth views of the global refining industry, including capacity data by unit and configuration, ownership status and history, and refinery-by-refinery crude slate, yields and outages data.

Oil inventory

Monitor and analyze this comprehensive global inventory database, covering detailed crude and refined petroleum inventories data - recent and historical. A combination of proprietary Analytics and third-party data, curated by S&P Global Energy, provides access to highly sought-after fundamentals.

Price assessments

Upgrade your vessel tracking service with the addition of S&P Global Energy (Shipping Service) to access essential cargo information on oil tankers as they leave a port including terminal of origin and destination, ETAs, quantity, grade, and charter party information to identify opportunities and trading decision and support commodity flows. Monitor volumetric crude oil exports and imports as it happens and discover shifting market trends before anyone else.

Forward curves

Manage energy price risk with a forward view of the market using Platts Forward Curves. Effectively calculate VaR, mark-to-market, fair values, and manage counterparty credit risk exposure. Markets covered include oil, power, natural gas, petrochemicals, NGL, LNG and coal in the Americas, Asia and EMEA.

Energy market insights

Get the latest commodity intelligence from S&P Global's editorial network, including confirmed trades, firm bids, offers, and transactional activity heard across the market. The team provides independent energy news and benchmark prices, helping you to make informed decisions.

Price assessments

Upgrade your vessel tracking service with the addition of S&P Global Energy (Shipping Service) to access essential cargo information on oil tankers as they leave a port including terminal of origin and destination, ETAs, quantity, grade, and charter party information to identify opportunities and trading decision and support commodity flows. Monitor volumetric crude oil exports and imports as it happens and discover shifting market trends before anyone else.

Forward curves

Manage energy price risk with a forward view of the market using Platts Forward Curves. Effectively calculate VaR, mark-to-market, fair values, and manage counterparty credit risk exposure. Markets covered include oil, power, natural gas, petrochemicals, NGL, LNG and coal in the Americas, Asia and EMEA.

Energy market insights

Get the latest commodity intelligence from S&P Global's editorial network, including confirmed trades, firm bids, offers, and transactional activity heard across the market. The team provides independent energy news and benchmark prices, helping you to make informed decisions.