My chats with clients have shifted recently, from what’s happening domestically, to action in global bond markets. As various economies emerge from the pandemic, there’s a potential cloud over the recovery. When interest rates rise, many emerging economies could see “significant” capital outflows, the IMF has warned.

Except for specific circumstances like Russia’s, emerging market bond yields are very U.S. driven. Commodity prices are far stronger than a year ago, and while this generally supports emerging markets, many have ramped up spending on pandemic mitigation efforts. In addition, several EMs are very reliant on tourism, which will take time to recover.

Of course, issues in these economies are varied and complex. Brazil’s national debt hit a record 90% of GDP in February, and its average daily death toll from the pandemic is now the world’s highest, with sovereign yields 75 bps higher this month. In China, turmoil at the nation’s largest distressed debt manager highlighted risks in its bond market - with many state-owned enterprises struggling to keep current with creditors. The firing of Turkey’s central bank governor has seen foreign investors pull ~$1.9 billion from domestic stocks and currency bonds, against a double-digit inflation backdrop. And Russia is expected to cut its 2021 borrowing plan after U.S. sanctions stop American banks from buying ruble-denominated state bonds. All up, the confluence of these political and economic risks means a global recovery could be increasingly bifurcated.

Closer to home, the $64 million dollar question remains: how well will asset prices hold up after stimulus and relief measures are eventually removed? Bulls note that pre-pandemic, U.S. economic fundamentals were strong, and that pent-up consumer demand may be some balm to imbalances like commercial real estate weakness and double-digit growth in some state budgets (hello, New York). Bears argue that government and central bank support has inflated asset prices beyond all fundamentals, allowing investors to use inflated assets in one sector (such as stocks) to drive up prices in others, such as housing. I look forward to your thoughts.

This article was originally published in Lynn Martin's Markets in Focus LinkedIn Newsletter.

Four things we’re watching

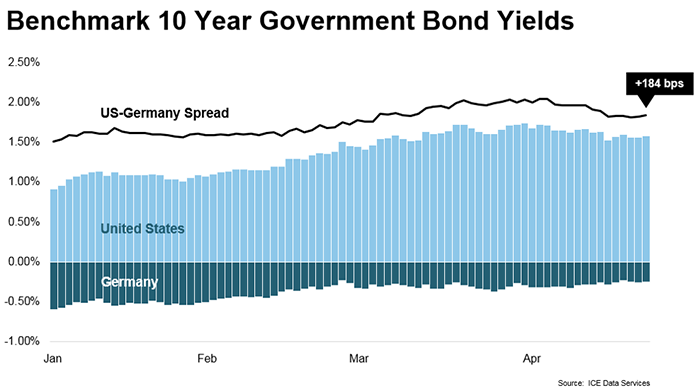

The spread between 10yr US Treasury and German Bund yields expanded by one basis point to +184 following the ECB’s vote to keep interest rates and bond buying unchanged. Investors will look ahead to the June meeting when policy makers are set to revisit the decision.

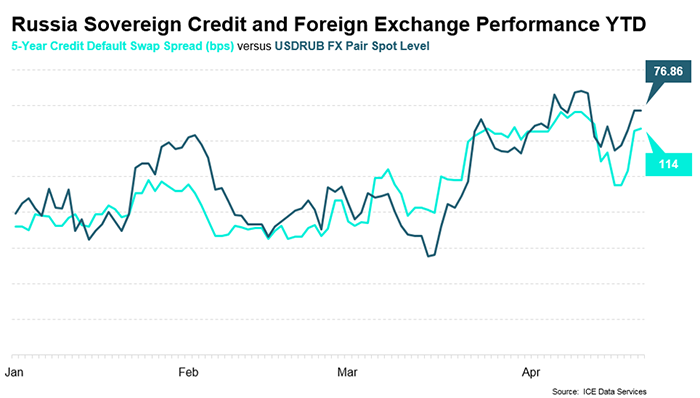

Russia’s sovereign credit risk and currency sit near the worst levels of the year.

Investors are monitoring the situation to see if further sanctions will be forthcoming in the wake of Vladimir Putin’s warning to western nations not to cross “red lines”.

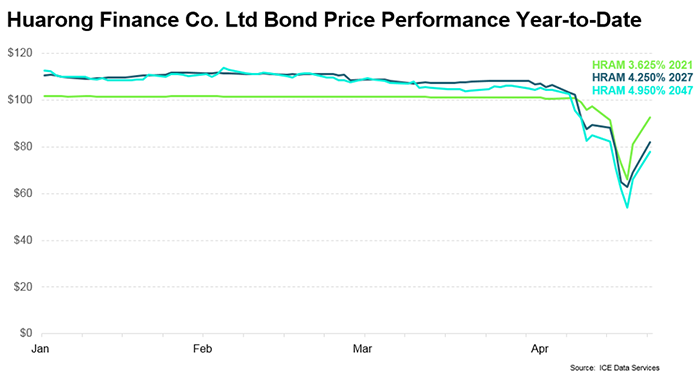

USD bonds issued by China’s majority state-owned Huarong rebounded +23 points on average after selling off earlier this month. Investor sentiment improved after the asset manager repaid a debt issue and assurance from the China Banking and Insurance Regulatory Commission.

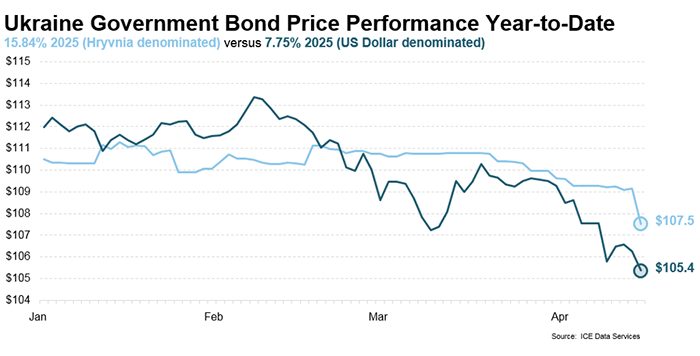

In the wake of Russia’s growing military presence in Crimea and other border regions, investor risk aversion toward Ukraine’s government debt is on the rise, leaving its bond prices near the lowest levels of the year, both for hryvnia and US dollar denominated issues.

Markets in Focus Newsletter