Participation in the derivatives markets

At a high level, there are typically three broad categories of traders in derivatives markets and, as markets have matured, many institutions can undertake a mixture of these activities:

• Hedgers use derivatives to reduce the risk they face from potential future price movements in a market and usually take opposite positions in derivatives in relation to their underlying physical position (e.g., a merchant with underlying long physical position due to commodity assets in storage would go short in the futures market to offset the price risk on the stored commodity);

• Speculators are market participants who use derivatives to take a position based on their views regarding the future direction of a market; and

• Arbitrageurs take offsetting positions across financial instruments to create a profit from price differences and movements in such price differences. This group is often referred to as Liquidity Providers.

With the types of market participants in the derivatives markets explained, it is important to draw a distinction between speculation and market manipulation. Market manipulation is illegal and impairs market functioning - and ICE has robust safeguards in place to prevent market manipulation as we will see later in this paper. Speculation, on the other hand, is an important and arguably an integral part of a well-functioning derivatives market.

Markets are shaped by a multitude of factors which influence price discovery in derivatives. They include geopolitics; conflict; the supply and demand of underlying commodities; international economic policy and growth; inflation expectations and currency valuations; energy policy; trade barriers; storage and transportation availability; and production capacity (such as OPEC and non-OPEC crude oil production, or refinery capacity). The prices of energy, commodities, and financial assets such as currencies across the world reflect the market’s collective view of all these dynamic factors that can influence a market and more - with fluctuations in prices arising as market and global economic conditions change.

Sharp fluctuations in prices of commodities and financial assets can create significant business challenges with adverse impact on production costs, operating margins, product pricing, earnings, and the availability of credit. As a result, there is value in the use of risk management and hedging instruments amongst commercial firms exposed to volatility in commodity prices, currencies, and interest rates.

The global futures markets such as those operated by ICE provide liquid, transparent platforms for businesses looking to hedge their price exposures across their value chains and across asset classes. It helps airlines make their fuel costs more predictable and helps oil refiners decide which fuels to buy and sell. Hedging helps businesses manage their cash flows more effectively allowing them to allocate investment for greener technologies, and secure financing for new investments. The banks and other financial institutions that provide the financing for these investments and the companies themselves require liquid futures markets to lay off the variety of price risks involved.

Exhibit 2: Case Study - Power Utility hedging using EU Emissions Allowance (EUA) futures

Source: Oxera, based on interviews with carbon traders

Consider a large power utility, which endeavors to meet the energy needs of its customers. This utility has many plants, with different energy types, and will use whichever plants it expects will be most efficient to meet demand. The utility anticipates needing to generate 10GWh of electricity in the near future to meet expected demand. It intends to generate 5GWh of this from gas plants, knowing that EUAs are required to cover the resulting emissions.

The utility then works out how many EUAs are required to meet that 5GWh gas volume. Once the utility has estimated how many EUAs it will need in the following year to cover its production, it has a choice: to wait until the permits are needed and buy the EUAs in the primary auction at that time, or to secure the required number of permits now on the futures market for its production in the following year.

Even if the utility has no knowledge about whether future EUA prices are going to increase or decrease, it might still choose to purchase the EUAs at the known futures cost in order to ‘lock in’ a price, thereby minimizing risk exposure and helping it to get greater certainty over its future margins.

The recent global energy price increases witnessed in 2021 and 2022 have highlighted the benefits of hedging and risk management for commercial entities. We have seen examples where firms that are well hedged have continued to operate, stay competitive and serve their customers. Ultimately futures markets contribute to protecting the end consumers from the adverse impact of higher prices.

Whilst commercial entities participate in the futures markets primarily with the objective to lay off their price risk, financial institutions, and other market participants willing to take the other side of their trades, bear the risk of price fluctuations and play a critical role in the provision of liquidity and price formation. Without the presence of market participants willing to take on the risk that commercial firms wish to lay off, businesses could be forced to raise prices to compensate for price risk they are unable to manage effectively.

Markets therefore require robust participation to enable the efficient transfer of risk and rely on a mix of commercial participants (looking to hedge their underlying price risk) and liquidity providers (usually financial participants or market makers). The proper functioning of markets, and indeed the enablement of hedging and risk management, can get severely impaired without the active participation of both groups. Put another way, financial participants perform an important economic function by providing liquidity and acting as additional buyers and sellers in the futures markets -- thus boosting market efficiency for the transfer of risk to take place.

The diversity of participation is better appreciated when considering the kinds of mismatches that can occur in a futures market between hedgers going long and hedgers going short. These can emanate in the form of a mismatch in quantity (e.g., more hedgers looking to go short than long), or a mismatch in timing (e.g., a hedger who wants to go long is unable to find a counterparty willing to go short at the same time), or a mismatch in contract maturities (e.g., a long hedger looking to buy six-month contracts is in a market where short hedgers are looking to sell one-month contracts). Under these circumstances, financial market participants come in to fill the void and fix such mismatches by acting as counterparties to hedgers looking to buy or sell futures in the desired quantities and tenors.

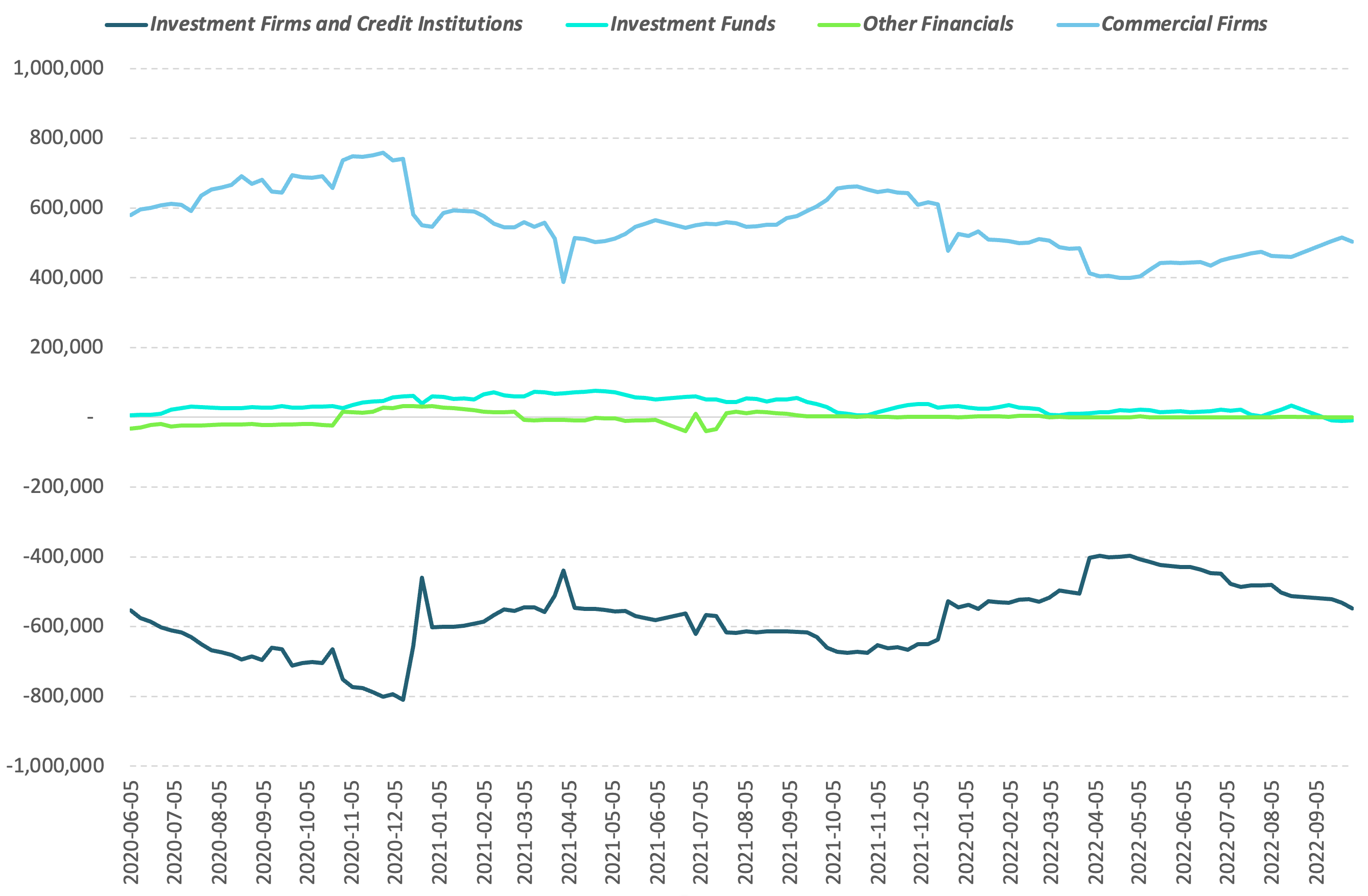

As an example, analysis of the Commitment of Traders (COT) reports for the EUA futures market at ICE, as seen in Exhibit 3, demonstrates that the largest trading positions are between financial institutions selling EUA futures against commercial entities that buy EUA futures with a view to hedge EU Allowance price and volume risk. This broadly aligns with the expected functioning of this market as commercial participants in the EUA futures market generally have emissions compliance needs under the EU Emissions Trading Scheme (EU ETS) and are therefore normally short in underlying EU Allowances. These participants predominantly take long positions in EUA futures that offsets their price exposure to EUAs while also helping many commercial participants secure EU Allowances to meet their compliance obligations (since EUA futures result in physical deliveries of EU Allowances upon expiration).

Exhibit 3: Net positions in EUA Futures by market participant type

Source: ICE Report Center, MiFID II Commitment of Traders Report

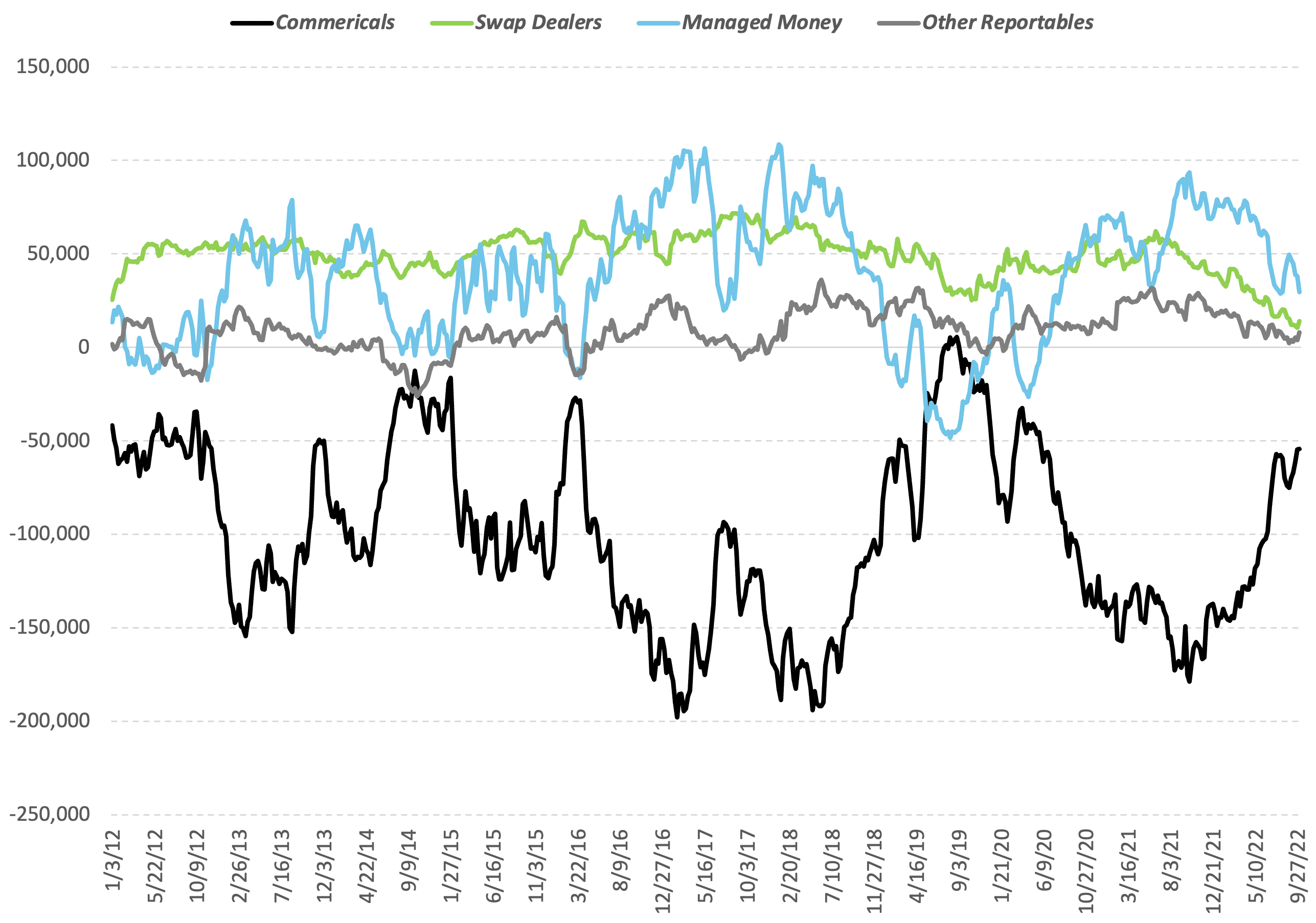

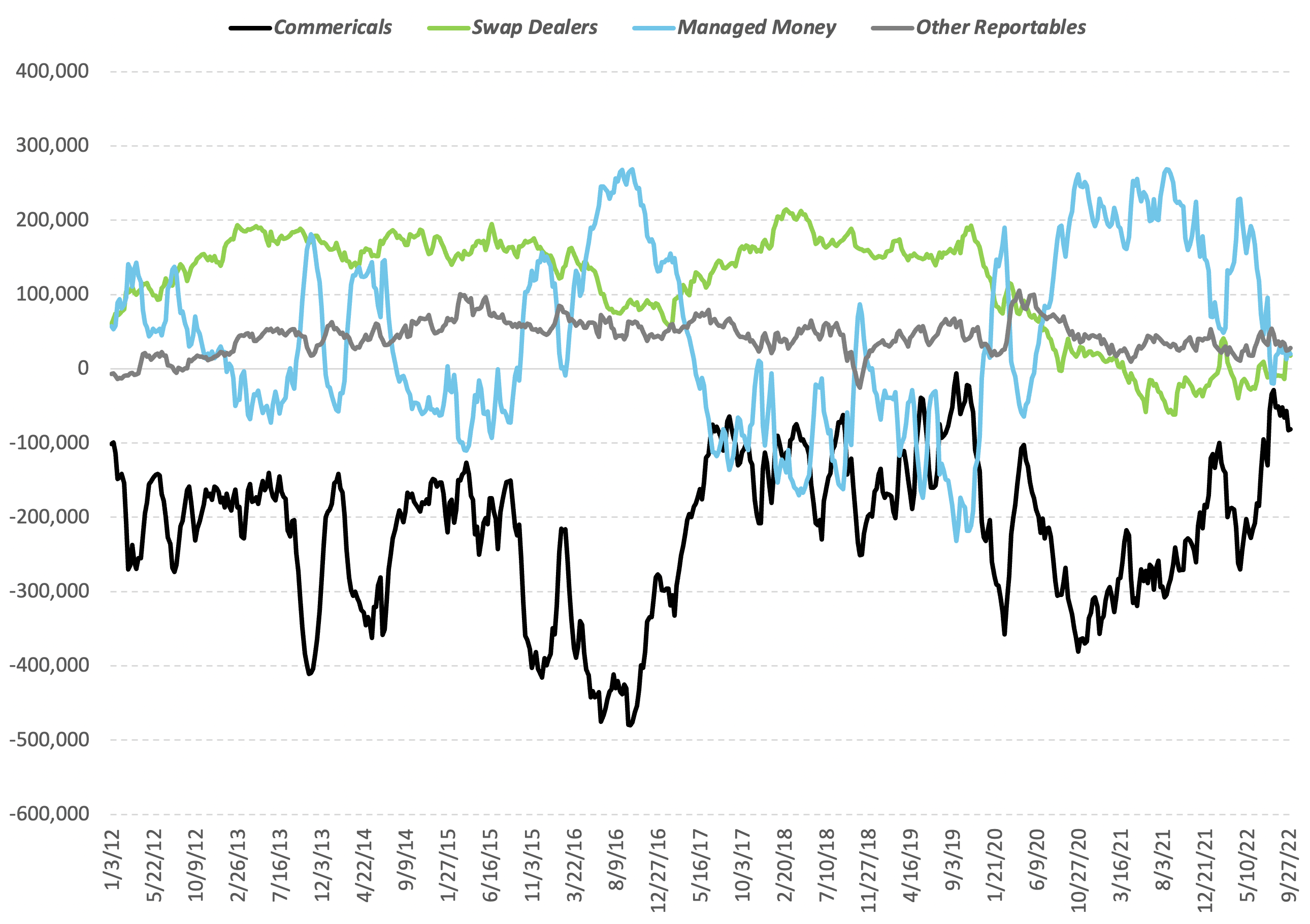

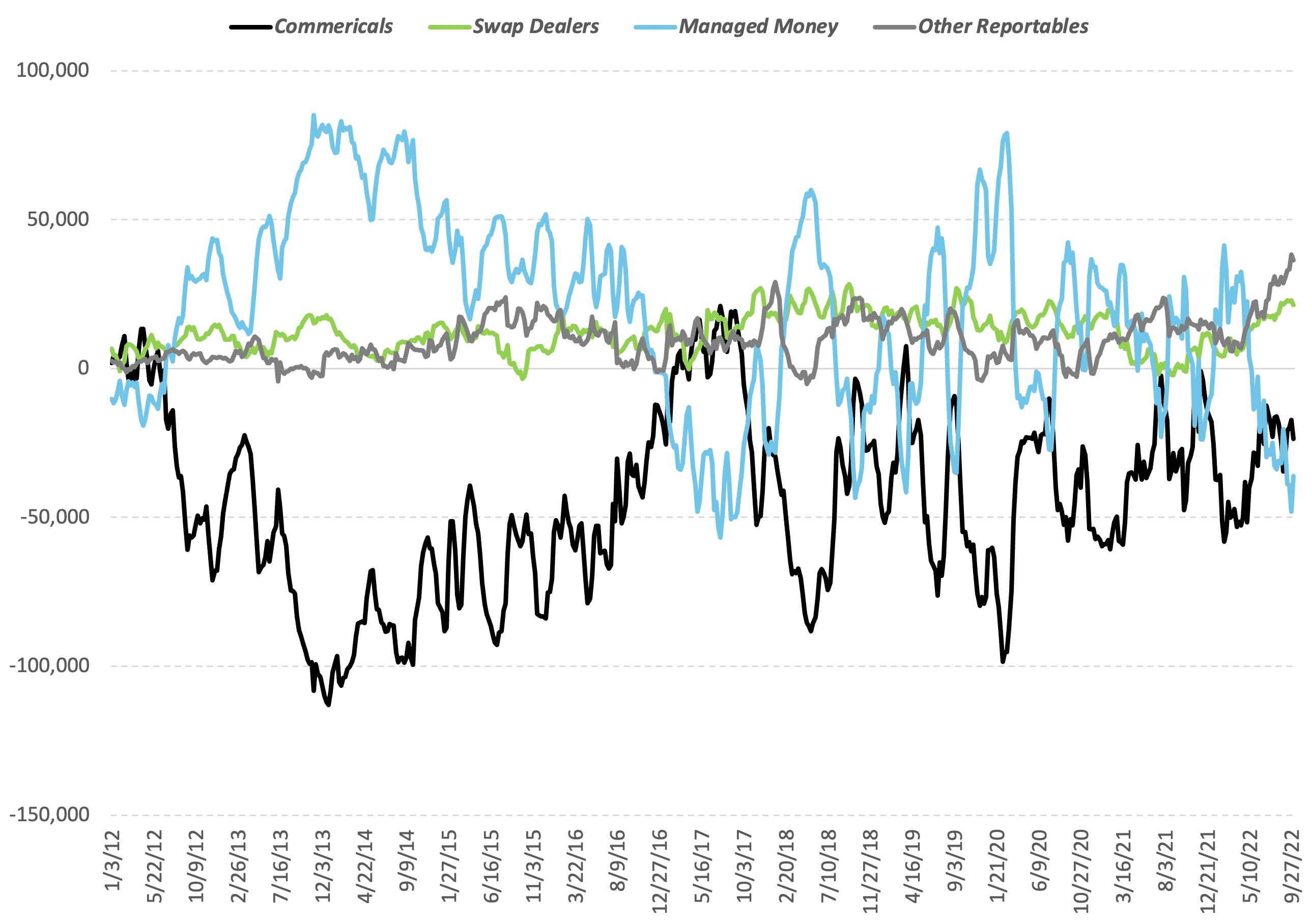

We can see a similar balance in the U.S. softs futures markets such as the sugar, cocoa, and cotton futures markets. Analysis of COT reports published by the CFTC over the last decade (as seen in Exhibit 4) shows that commercial participants tend to hold the bulk of net short positions with financials being the net longs. This reflects the dynamic of commercial firms in these markets -- which include producers and merchants -- relying on financial participants to assume the risk they need to offload in the futures market and therefore hedge their underlying long positions in the physical commodity. The presence of both groups in these markets allows commercials to reduce their risk exposure, and for the financials to assume that risk, enabling efficient and cost-effective transfer of risk to occur between counterparties.

Exhibit 4: Net positions in the U.S. Softs Futures markets by participant type

Source: Commodity Futures Trading Commission

(a) No. 11 Sugar Futures

(b) Cocoa Futures

(c) No. 2 Cotton Futures