As the executive summary explains, the purpose of this report from Energy Intelligence is to provide a deep dive into the role of the Brent and West Texas Intermediate (WTI) crude oil benchmarks, their mutual relationship, and their interaction with the global oil market.

Part three closes out the series with a focus on Brent: its evolution, its markets and why its ecosystem is relied upon by commercial and non-commercial participants alike.

Brent the global benchmark

Overview

The longevity of Brent as a benchmark stems from its ability to create and maintain liquidity through the multiple layers of its pricing complex. Since the first Brent cargo traded in 1983, what was originally an over-the-counter (OTC) market dovetailing with the North Sea boom has expanded into a full suite of instruments attracting an ever-broader gamut of investors and open interest. The various layers of the paper and physical markets feed into each other and create a resilient ecosystem. No single price can represent hundreds of distinct qualities of crude in the world. But nearly two-thirds of the spot export market is linked to Brent.

Brent futures started to trade on the International Petroleum Exchange — now ICE — in June 1988. Like other commodity markets, Brent needed standardization to generate further trading volumes and improve price transparency. Its physical forward and futures contracts were initially seen as competing instruments, and it was thought that futures would find a wider appeal and take precedence. For Brent, they turned out to be complementary.

By design, Brent has cargoes physically delivered with an option to financially settle. For the market, Brent is primarily a physical benchmark. Throughout the years, however, Brent’s position as the world’s physical benchmark has been called into question by a dwindling physical base, prompting several changes. Natural production declines have continually dried up liquidity in the Brent forward contract and spurred a series of remedial fixes, such as the addition of new streams and the introduction of quality differentials. The lack of tradable volumes has remained an issue that needs constant attention.

The number of North Sea fields underpinning Brent has risen from just one to about a hundred. Brent has also become more of a financial instrument as it responded to the evolving hedging and risk capital needs of increasingly sophisticated players, which added complexity but elicited more trading volumes too.

Among the complex’s various layers, Brent futures have been key to achieving liquidity. Many participants came to the futures market to manage risk, rather than acquire Brent crude. Futures also drew in managed money, taking on the risk that hedgers are laying off. As open interest in Brent futures increased, so did the ability to hedge price exposure effectively, building up liquidity in the longer-dated contracts.

- In recent months, we’ve seen proposed changes to the way the physical Dated Brent benchmark price is assessed. These changes could be fundamental and far-reaching, and have generated robust market discussion. As Dated Brent is a key component of the wider Brent complex that includes ICE Brent Futures, it’s useful to provide perspective for ongoing market discussion.

- This installment from our Energy Intelligence series examines the evolution of the Brent benchmark since its inception in the 1980s. Production in the original Brent field peaked in 1984, and its evolution includes adding new crude streams and introducing quality differentials, among other changes. Brent is currently comprised of a basket of five different North Sea grades: Brent, Forties, Oseberg, Ekofisk, and Troll (BFOET).

- Through an in-depth analysis of the Brent “ecosystem”, this chapter examines the functioning of its four layers. These comprise: the markets for Dated Brent (the physical spot market); Brent Forwards (the physical forward or “cash” market); Brent Futures; and Brent swaps and options (OTC Brent derivatives).

- There’s also a detailed discussion of interlinkages between the different layers. These families of instruments include: contracts-for-difference (CFDs), which connect Dated Brent with the Brent Forward market; the Exchange of Futures for Physical (EFPs) which strongly link the Brent Forward physical market with the Brent Futures market; and Dated-to-Frontline swaps (DFLs) which set a price differential between Dated Brent and the front-month Brent Futures contract. Links between Brent and other benchmarks including WTI and Dubai, are also covered.

- Finally, this chapter describes how components of the Brent ecosystem — the layers and their interlinkages — are used by commercial participants to hedge and manage risk, and managed money participants to invest and take risk.

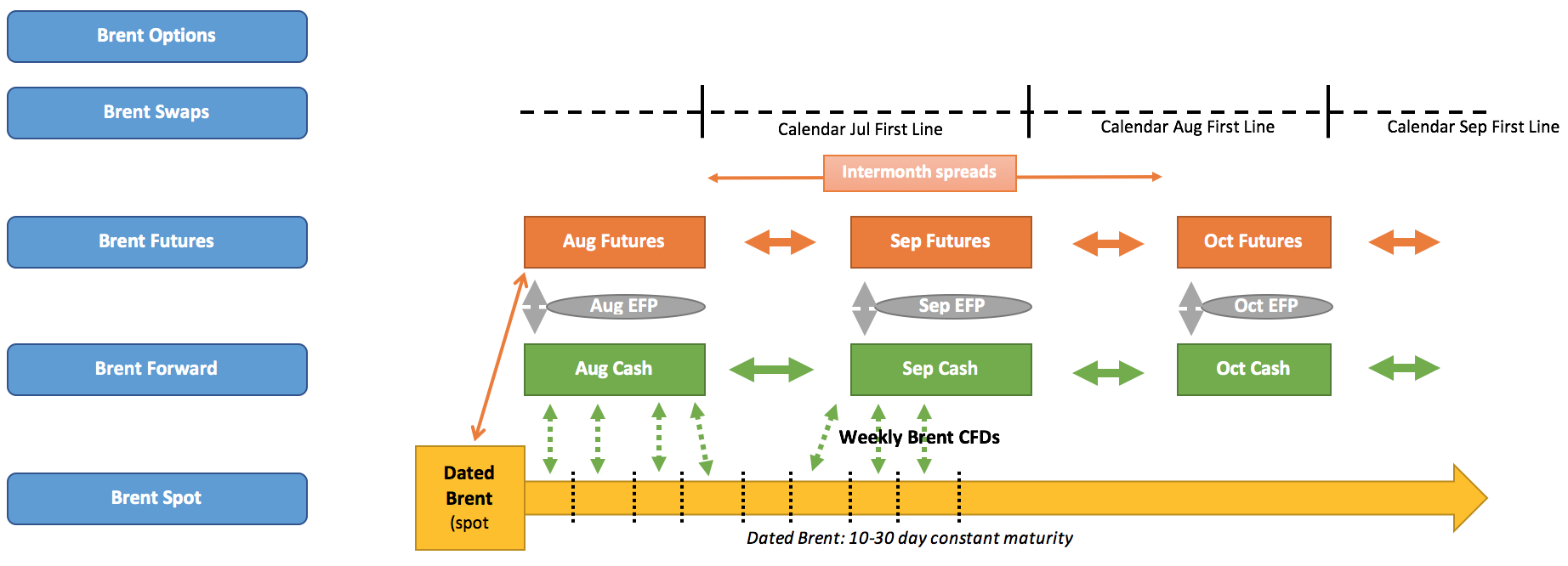

The Brent complex

To the general public, there is just one price of oil. But the oil market sees — and needs — lots of prices. Brent was designed to price barrels of light, sweet oil produced in the North Sea region. But all crudes are different. Therefore, all barrels linked to Brent are universally priced at a differential to it, depending on their availability and their relative quality. To put it simply, the Brent ecosystem itself can be divided in four layers: the spot market of dated Brent, the forward market, the futures market and the swaps and options markets. The world sees the futures price as the price of oil. The trade uses all of them.

In the Brent market, the physical price — known as dated Brent — is discovered in the forward and futures markets. As Brent complexity built up, the interlinkage between paper and physical markets became deeper. Yet, a recurring fear stemmed from Brent’s falling liquidity and ability to adequately reflect supply and demand. That fear goes all the way back to 1984 when production in the eponymous Brent field peaked, threatening to dry up liquidity into the physical and forward market. The answer was to comingle output from the nearby Ninian field with Brent. It was renamed Brent Ninian Blend in 1990. This solution was repeated ever since. Forties and Oseberg were added in 2002, followed by Ekofisk in 2007 and more recently Troll in January 2018.

The inclusion of additional streams into the original Brent benchmark brought two major transformations. The first is that Brent became a basket of different light, sweet grades rather than a single crude: Brent, Forties, Oseberg, Ekofisk and Troll (BFOET). The second transformation was the introduction of quality premiums (or discounts) against the Brent stream by price reporting agencies to compensate for the delivery of any of the BFOET grades that is not Brent itself.

The Forties stream alone is a blend of crudes flowing from 70 different fields, including the sour Buzzard stream. The latter made up 28% of Forties in 2019 and has contributed to a substantial increase in the grade’s sourness. Being lower in quality, Forties is in theory the cheapest grade to deliver. Since the cheapest BFOET cargo traded in the 4 p.m.-4:30 p.m. London trading window also sets the price of dated Brent, Forties ends up setting Brent spot prices most of the time. It is the dated Brent price that the world’s spot traders look at for pricing their cargoes.

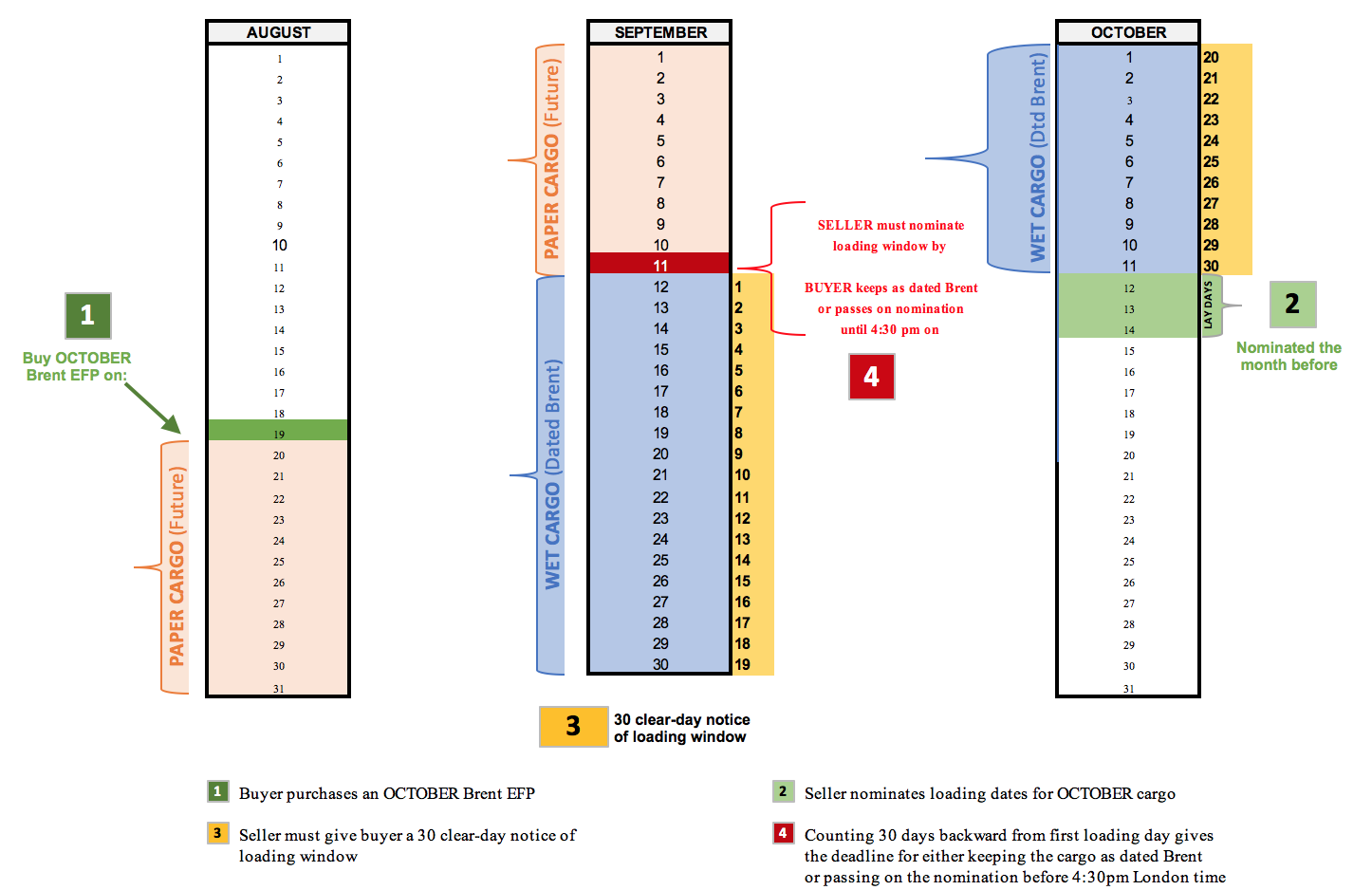

The physical or spot market for nominated BFOET cargoes thus constitutes the first layer of the Brent benchmark. Its parent market is the forward Brent market where, once a forward Brent cargo has acquired a vessel and a three-day loading window, it becomes dated Brent. Cargoes of dated Brent have a constant maturity of 10-30 days — not to be confused with the forward market. Sellers of spot cargoes must give buyers at least one calendar months’ notice of their loading window, owing to the practicalities of finding, vetting and chartering a tanker and coordinating with the oil terminal. Hence, even Brent spot trading includes a necessary element of forwardness to give buyers contractual flexibility.

Brent first traded as a forward market in OTC bespoke contracts, which was quicker to establish than a futures market from a regulatory point of view in the early 1980s. After 1988, it was thought that Brent futures would eventually replace the Brent forward market completely. Nowadays, new futures contracts are easier to launch and would be the first port of call for an exchange. Unlike Brent futures, forward contracts must go to physical delivery. Today they survive and coexist with Brent futures, mostly through the addition of hedging instruments in the Brent toolbox.

The Brent forward market deals with cargoes that load at least one month in the future. Neither the actual loading dates nor the specific grade of the cargo are known at the time of the transaction. Brent forward contracts are based on the principle of chains: Once a BFOET equity producer has nominated a buyer, this buyer must accept the nomination and load the crude or pass the nomination onto another buyer.

As a result, daisy chains of contracts are formed until a party decides to take delivery. Buyers can book out their paper position until a loading date is attached to the forward cargo, which then becomes wet. If a circular chain — or loop — is identified, a cash settlement can be agreed. Once wet, the cargo must be sold as dated Brent.

The Brent forward market was successful for two reasons. First, Brent started to trade in forward deals in 1983 and rapidly fostered liquidity into longer-dated contracts, from mostly month and month+1 deals to month+4 deals by mid-1985. This allowed the industry to rapidly meet hedging needs despite futures markets being hampered by regulatory requirements.

Second, the Brent forward market lifted its high entry barriers by allowing investors to trade smaller parcels for hedging or speculation purposes. Brent partials were introduced in 1986. They were originally linked to an OTC hedging concept allowing buyers to price their forward trades in tranches of 50,000 barrels at prearranged trigger dates.

Brent partials are very similar to futures, but with a stronger connection to the physical market. Unlike futures, they price physical barrels and can therefore end up in a physical cargo delivery once a buyer has collected six partials of 100,000 bbl each, or a full 600,000 bbl cargo.

The natural step to Brent futures, which constitutes the third layer of the Brent ecosystem, is the regulation of what already existed in the forward market. Brent futures are sold in standardized lots of 1,000 bbl and trade predominantly on ICE Futures, where contracts are margined and subject to margin calls. The exchange acts as a clearing house between buyers and sellers, eliminating counterparty risk.

Historically, less than 1% of future contracts go to physical delivery, which is true for Brent but also for physically delivered West Texas Intermediate (WTI). The majority of investors are unwilling to take delivery of 600,000 bbl of North Sea oil, and delivering partials in 1,000 bbl lots is impractical. Therefore, the ICE Brent futures contract provides an option to cash settle against the ICE Brent Index at contract expiry (last trading day of contract month).

The Brent loading schedule: from paper to wet

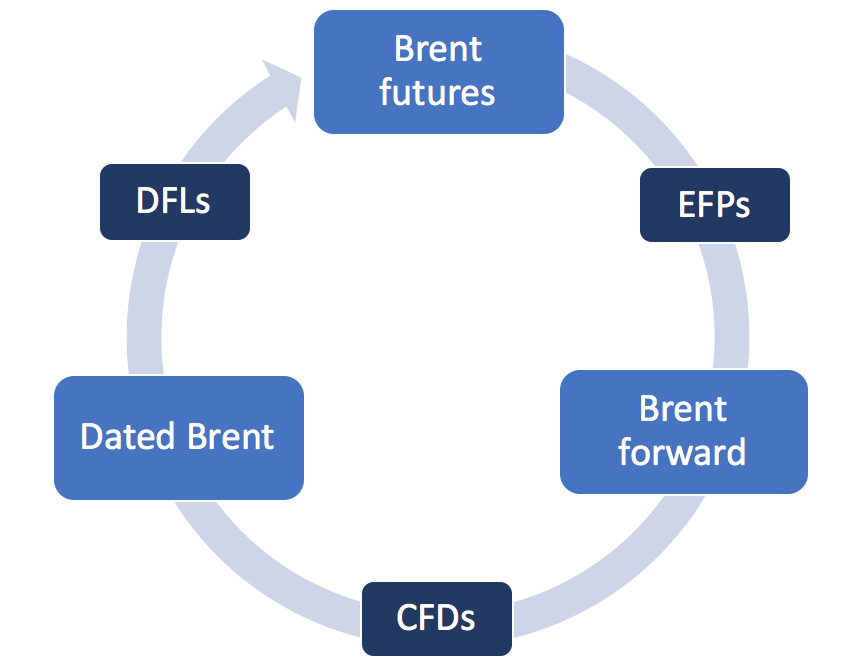

Often referred to as OTC Brent derivatives, Brent swaps and options constitute the fourth layer of the Brent complex. Although swaps are usually not established as an integral part of the oil market, they have proved ideally suited to the Brent market and have developed rapidly. The most important family of swaps for Brent is the contracts-for-difference (CFDs),which essentially connects the forward and futures markets to dated Brent.

The Brent dated-to-frontline (DFL) swaps, which set a price differential between dated Brent and the front-month Brent futures contract, are a variation of Brent CFDs. Like CFDs, DFLs allow traders to observe and pin down the value of price relationships between the physical and derivative markets, in particular the constantly changing prices at prompt points of the forward curve, where supply and demand are relatively inelastic. Because of this inelasticity, a change in market conditions has an immediate effect on spot prices as physical markets need to rebalance, and this is reflected in those swap values.

To hone the whole system, the Exchange of Futures for Physical (EFP) provides an elective mechanism that enables holders of ICE Brent futures to go to physical delivery at the time of their choosing — as opposed to expiry day only. A futures position can be transformed into a physical one without the need for immediate cash settlement. The EFP introduces a strong link between physical and futures prices by allowing two participants in the Brent futures and Brent forward market to switch their positions.

The Brent constellation

Brent's Appeal

Brent is a seaborne benchmark that can easily move supply out of its production region to take advantage of more favorable economics in other parts of the world. It trades on a spot basis and is considered a good reflection of global market fundamentals, responding to wider price-moving events such as supply disruptions, inventory changes, geopolitics or financial events. The various layers of the Brent complex allow for a variety of players to react to the global price of oil and to their needs.

Option to Cash Settle

Brent futures can be cash settled and are not designed for physical delivery. Delivery is possible if both the seller and buyer wish so, but Brent futures contracts still open at expiry must be settled in cash against an index price derived from the physical market. The contract was designed this way because of the difficulties in matching the physical delivery procedures with a realistic futures market.

Because the prices of forward and futures contracts can diverge from those of the underlying commodity as expiry nears, they must converge through a physical settlement mechanism. Brent is physically delivered via the EFP mechanism, with an option to cash settle for participants who do not wish to take delivery of a 600,000 bbl crude cargo. At expiry, the buyer of a forward or futures contract wishing to take delivery will hence receive physical oil at the same time and under virtually the same conditions as a buyer on the physical market. The purpose of providing for delivery on the futures contract is to cause convergence of the futures price and the cash price during the delivery period, both prices being not necessarily equal prior to the delivery day. This convergence also provides a basis for Brent futures pricing and allows them to serve as an appropriate hedging vehicle for cash market participants.

Because the prices of forward and futures contracts can diverge from those of the underlying commodity as expiry nears, they must converge through a physical settlement mechanism. Brent is physically delivered via the EFP mechanism, with an option to cash settle for participants who do not wish to take delivery of a 600,000 bbl crude cargo. At expiry, the buyer of a forward or futures contract wishing to take delivery will hence receive physical oil at the same time and under virtually the same conditions as a buyer on the physical market. The purpose of providing for delivery on the futures contract is to cause convergence of the futures price and the cash price during the delivery period, both prices being not necessarily equal prior to the delivery day. This convergence also provides a basis for Brent futures pricing and allows them to serve as an appropriate hedging vehicle for cash market participants.

CFD Swaps

Because CFDs connect the Brent forward market to dated Brent, they do most of the stretching when market conditions change. CFDs enable companies buying or selling barrels priced off dated Brent to control their exposure to the fluctuating spread between dated Brent and the paper Brent forward market. The purpose of hedging is to create certainty about the price, like an insurance. Since Brent cargoes are priced five days around the bill of lading, CFDs — which are traded for weekly delivery periods — give market participants the optionality to select a specific five-day period and achieve a riskless, guaranteed profit by fully hedging their position.

The Brent Constellation

Source: Energy Intelligence

Originally conceived as a bespoke hedge, the introduction of Brent CFDs increased the Brent market’s liquidity by offering new trading opportunities to pure risk capital. This money could bet on the volatility of the differential between dated Brent and the Brent forward market.

Link to Other Benchmarks

Brent’s wider appeal with investors has also been fostered by its linkage to other crude pricing benchmarks, notably WTI in the US that prices light, sweet US oil, and the relatively liquid Dubai swaps market, which effectively prices spot volumes of Middle Eastern crude East of Suez.

The Dubai price is connected to Brent through the Exchange of Futures for Swaps (EFS) spread, which represents the differential between Brent futures and the Dubai cash market. The so-called Brent- Dubai EFS is underpinned by the Dubai intermonth swap spreads.

The Brent-Dubai spread is one of the main criteria that dictates the viability of physical arbitrage between the Atlantic Basin and Asia. A weakening of the EFS would signal that any sweet crude produced in the Atlantic, including not only North Sea oil but also West African crude, is starting to move East of Suez.

Continued Success of the Forward Contract

Although Brent futures have become the first point of reference for traders, their relationship with the forward market is almost symbiotic. Brent futures have grown out of the forward market liquidity, and it is the forward market that takes Brent futures to dated Brent through the obligation of physical settlement. Unlike futures, Brent forward contracts enable companies to trade larger volumes in a single transaction, to choose their trading partners— as opposed to being matched by an exchange algorithm — and to trade round the clock outside of ICE Futures exchange hours.

Hedging Basis Risk

For participants wishing to make a physical transaction without being tied up to a specific grade, delivery point, or who simply want to choose their counterparty, the Brent EFP mechanism offers an option to do so. Besides providing a valuable hedging instrument, the paper Brent forward market also provides a better hedge for companies operating outside of the US. In Asia, partial Brent trades are still popular because they allow companies to trade smaller parcels of oil.

Comingling Benchmarks

Despite different upstream economics — Brent is extracted offshore, WTI onshore — both crudes register as light, sweet oil. Yet both markets respond to different storage and transportation logistics and, until December 2015, WTI was a landlocked crude owing to a US ban on crude oil exports. This created price discrepancies and drew speculators in.

Trading the Spread

ICE Brent futures share the same size and one-cent increment value of Nymex WTI futures. Spread trading between the two contracts was thus relatively easy to implement. The WTI-Brent spread quickly gained in popularity and still accounts for a large volume of futures trading.

Until a decade ago, both prices moved in tandem most of the time, making the spread relatively predictable. WTI was trading at an average $1.50 premium to Brent. That premium paid for grades similar in quality to WTI to be shipped from the North Sea or West Africa to the US and land at comparable costs. However, when US tight oil started hitting the market in force in 2011 just when Canadian supplies pushed US oil towards the coast, the spread’s volatility levels increased dramatically. The amplitude and frequency of changes in the spread became higher, decoupling Brent and WTI prices.

Rise as a Benchmark

Brent has gained wide adoption beyond the North Sea. Most crude grades produced in the Atlantic Basin are explicitly linked to Brent through their price formulas, while many Middle Eastern grades are implicitly linked to Brent through the Brent-Dubai EFS spread.

Despite being a medium, sour grade, Russia’s flagship export grade Urals (or Rebco) is priced against dated Brent too. Brent has found some appeal with other producers as well because of its seaborne nature and ability to easily move out of its production region.

Related content

RESEARCH REPORT

Global crude benchmarks: Brent sets the standard

Part 1

In their executive summary, Energy Intelligence explores the role of Brent and WTI crude oil benchmarks, their mutual relationship and their interaction with the global oil market.

Research Report

Global crude benchmarks: Brent sets the standard

Brent Sets the Standard Part 2

Part two of the series delves into why the world need benchmarks and what characteristics they obtain.

Article

Brent: the world's crude benchmark

Learn how this crude became the epicenter for world crude and now prices 78% of global oil.

RESEARCH REPORT

Global crude benchmarks: Brent sets the standard

Part 1

In their executive summary, Energy Intelligence explores the role of Brent and WTI crude oil benchmarks, their mutual relationship and their interaction with the global oil market.

Research Report

Global crude benchmarks: Brent sets the standard

Brent Sets the Standard Part 2

Part two of the series delves into why the world need benchmarks and what characteristics they obtain.

Article

Brent: the world's crude benchmark

Learn how this crude became the epicenter for world crude and now prices 78% of global oil.